Financial Literacy: The Costly Mistake Everyone Makes with Rich Dad Poor Dad (Book Review)

Robert Kiyosaki

Rich Dad Poor Dad: What the Rich Teach Their Kids About Money That the Poor and Middle Class Do Not!

Rich Dad Poor Dad uses the conflicting financial advice of two father figures to spark a radical cognitive shift regarding personal wealth. The fundamental lesson is that readers must understand the strict mathematical distinction between an asset, which puts money into your pocket, and a liability, which takes money out of your pocket. Ultimately, the book argues that the middle class remains trapped in a cycle of paycheck dependency because they unknowingly purchase liabilities, whereas the wealthy adapt and achieve total autonomy by systematically building businesses and acquiring assets that generate passive income.

Weekly Challenge Trophy Legendary Weekly Challenge

Take intentional steps toward shaping the life they want.

Here’s what to do:

- Sit down and list out how you want your life to look.

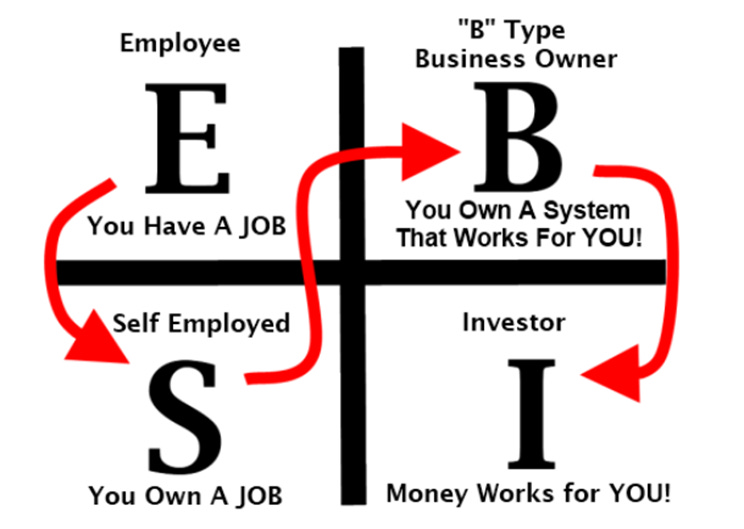

Think about the type of employment you want, do you want to stay an employee (E), maybe move over to self-employed (S), or dabble in business ownership (B) and investing (I), or a combination? Decide what fits you best.- If you have a spouse or partner, talk about your plans together.

Each person should share their own goals, then find ways to align and create a joint plan for your family or partnership.- Take one small action right away.

This could be putting a reminder on your calendar, making a phone call, opening an account, ordering a relevant book, whatever moves you closer to your goal.- Every day, commit to one step forward.

Keep the momentum by taking daily action, even if it’s small.The goal is to move from planning to doing, so you’re actively creating the future you want.

SELECTED LINKS FROM THE EPISODE

Visit RichDad.com for books, the game, and more resources for your financial education.

Rich Dad Classics Boxed Set

CASHFLOW Board Game

CASHFLOW Board Game Online Edition

Rich Dad Media Network Podcasts

Cashflow Quadrant

Two episodes we did, breaking down the Cashflow Quadrant's

Rich Dad Poor Dad Lied To You by Codie Sanchez

Jasmine DiLucci | Tax Attorney, CPA, EA

MONEY Master the Game: 7 Simple Steps to Financial Freedom (Tony Robbins Financial Freedom Series)

Failing Forward: Turning Mistakes into Stepping Stones for Success

Making Liabilities Assets

Pejman Ghadimi - The man who invented hacking liabilities into assets

Episode Transcriptions

Show notes and transcripts powered with the help of Castmagic. Episode Transcriptions Unedited, Auto-Generated.

Tyson Gaylord [00:00:02]:

Welcome to Social Chameleon show where our goal is to help you learn, grow and transform on your path to becoming a legendary today. What I got wrong from the Rich Dad, Poor dad book. So I was always under the impression that the whole book, the whole point of the book was just by real estate. And that's because I never actually read the book. I just listened to people who had. I went to meetups, classes, courses, conventions, the whole thing. I'm sure you guys remember probably especially in the early 2000s, I was just, at least where I lived, it was a big thing. It was always some real estate class, seminar, whatever.

Tyson Gaylord [00:00:41]:

And if you go back to the previous episode, I linked that about, you know, I didn't read books. I wasn't, I was self conscious about it and whatnot. I talk about it in the episode. And so because I never actually read the book entirely, I read parts of it here and there and whatnot and stuff. So I completely missed to me the core lesson and I finally reread it. Technically, I listened to the audiobook and I had an aha. Like, oh my God. This whole time I missed the entire point.

Tyson Gaylord [00:01:14]:

So it was always, you know, every. Everything I knew about it prior to fully reading it was. It was just everything. Whatever you had to do, just buy real estate, just buy rental properties, get rental properties, get rental properties, right? And it was always, it's difficult, right? You know, yeah, there's ways to do it. Little or no money. There's ways to partner people and all these things. And you know, a lot of industry was kind of built around, around people not really understanding and not under, not reading the whole book. So in this episode, I'm going to go over, you know, my lessons and takeaways from the book.

Tyson Gaylord [00:01:50]:

I'm going to also go over the common criticisms. There's plenty of videos up, you know, on YouTube and whatnot and different things of people tearing this apart. And I kind of want to talk about some of that too. And ultimately, what the. I think this is the takeaway for me what I, what I finally learned after all these years of the book and some interesting things, I guess, about books, right? This is so like Naval Ravikant said, the point of reading is to guide your own thinking, not to take on someone else's thinking. Ralph Waldo Emerson wrote in his essays that books are for nothing but to inspire and that one's own creative thinking is the ultimate goal of reading. Most people spend their entire lives working for money instead of building systems that make money for them. This book shatters the illusion that that high salary equates to wealth.

Tyson Gaylord [00:02:41]:

I'm sure plenty of us know people that make a lot of money and are still living paycheck to paycheck. So now, by forcing you to confront the mathematical distinction between assets and liabilities, if you want to escape the cycle of paycheck dependency, you must completely rewire your view of your personal cash flow. And this is what ultimately taught me, this book taught me and what really resonated with me when I first heard of this book. I believe it came out in 1997. This is an updated version with some newer things in it. My, my old copy was just pretty, pretty tattered and worn. But it resonated with me because I. To not sound trite or purposely contrarian or whatever it is, I.

Tyson Gaylord [00:03:25]:

I just don't think about things the way normal, I guess, quote unquote, normal people think or regular people think about it, things. And, and there's always been a hard disconnect with me because I, you know, I always thought so when I find books like this, like, even like Tim Ferriss's Four Hour Work Week, I'm sure we're going to get into a little bit of that as well. With these different types of thinking. It aligns with how I feel like I'm thinking about how my brain works and helps me gather my thoughts. So this is what, you know, initially got me liking this book. And then as we'll talk about going down the wrong road because I never actually read the book. Quick thing. If you're not familiar with the book, Richard Poor dad uses the conflicting financial advice of two father figures to spark a radical cognitive shift between shift.

Tyson Gaylord [00:04:10]:

Regarding personal wealth, the fundamental lesson is that readers must understand the strict mathematical distinction between an asset which puts money in your pocket and a liability which takes money out of your pocket. This is this core. That core sentence to me was like the most profound thing I first heard about. I was like, wow, what a simple concept, right? Asset liability, it's always, you know, feels a little weird, but simple, right? Assets put money in your pocket. Liabilities take money out of your pocket. Super simple cognitive mental framework, right? Ultimately, the book argues that the middle class remains trapped in a cycle of paycheck dependency because they unwillingly purchase liabilities. Oh, sorry. Unknowingly, maybe even unwillingly unknowingly purchase liabilities.

Tyson Gaylord [00:04:55]:

Whereas the wealth adapt and achieve total autonomy by systematically building businesses and acquiring assets that generate passive income. Robert Kiyosaki is a polarizing entrepreneur. He's a author of this book. He's a polarizing entrepreneur and investor who challenged conventional financial wisdom by introducing the cash flow quadrant. We did a whole two episodes on that. If you want to go back and check that out. I'm not going to get into a ton of that. We did episode 9 and 10.

Tyson Gaylord [00:05:22]:

I'll link that for you guys. You can understand and get a feel of cash flow quadrants. In the book, he contrasts his highly educated father's traditional advice with the street smart business acumen of his best friend's entrepreneurial father. The narrative shows how the wealthy systematically acquire income producing assets. Although middle class unknowingly accumulates liabilities. Kiyosaki used his philosophy to shift to build a global education empire. Yet his tactical advice often draws criticism from financial professionals for being simplistic, speculative, and sometimes legally risky. And, and we'll get into a lot of those criticisms.

Tyson Gaylord [00:06:02]:

I'm not glossing over that. I'm not, I'm not hyped, man. For this book. I think there's great things in here and there's also times use your brain. Don't be a useful idiot. Okay? The things right off the top that I, that this book taught me and to this day it still goes in my mind. I taught my kids these things. I try to share them with others as well as I think these, you know, we can go with the whole cliche.

Tyson Gaylord [00:06:27]:

The school system doesn't teach us this because the school system is not designed for that. And that's okay. But you need, we need to educate ourselves. This is what happens outside of school time, outside of work hours. You need to educate yourself on protecting yourself because the only person that cares about you the most is you. So it's your responsibility. It might not be your fault, but it's your responsibility to get shit going. Having money for investing, right? These are the things we need money, right? If you want to do these things, whether whatever the capacity is the money you save, whether it's access to other people's money, which is a concept I learned from this book and whatnot.

Tyson Gaylord [00:07:07]:

And other people can be whatever friends, relatives, other investor types. It could be the. In America, the Small Business Administration, SBA gives out grants. There could be other grant organizations, other scholarships, loans, understanding where money is, how to get it, whatever. That's maybe even just step one, right? Just having the mental thing to know money's out there, I need to figure out how to get it, whichever way that is. And then, you know, having money to buy things, what, what is that like? Right? Making sure you know you're not going broken, you're going in debt and stuff like that to, to buy things, right? You know, you know, the classic examples, you know, cars and watches and handbags stuff, those can be arguably those are, if you buy correctly, there are assets, there are cars, there are bags, there are watches, there are collectibles, there are things bought correctly. When you understand these things, those things are liabilities. They're, they're bought, you know, but if they're bought from the purpose of their assets, they are assets.

Tyson Gaylord [00:08:12]:

They can be assets, they're appreciating assets, right? Whether that's just because of inflation or that's because of the nature of the items, the scarcity, the speck of things or whatever it, whatever it be, right? Understanding is. But having money to buy these things, you need that, right? And also something I never really thought about, you know, whatever, whatever the reason. Maybe my parents didn't talk about it, whatever. Definitely schools and stuff, they come up. But having money for emergencies. I remember when I was early on in life and friend of mine was in a tragic accident, he lived in different state. I didn't have money to go, you know, some of my friends did. And I was tank, never want this to happen again, right? And this is something, you know, I should have taken advice from, this book is having these emergency funds, having these different things, right? They say in America the average person doesn't have whatever it be.

Tyson Gaylord [00:09:00]:

There's a couple different things. 4 or 5, $600 in case of an emergency, right? And in my case, that was the thing. I didn't have four or five hundred bucks, whatever it was, to get an airplane ticket and go see my friend that was in a tragic accident. I felt some kind of way about that. I felt a little bit guilty and like, how stupid was that, right? So that's something I picked up from this. And understanding the difference between I can't afford this and how can I afford this. These seem like semantics, right? It's all this. You're saying the same thing.

Tyson Gaylord [00:09:31]:

You're not saying, saying the same thing. Your brain doesn't understand the. You're telling yourself, right? Like if you're telling yourself, I can't afford this, I can't afford this. But maybe, you know, I figured, I mean, no, you, you've already set yourself down the wrong path. This is. You're starting off with the negative, right? We can't start with the negative, you know, versus how can I afford this now? What does your brain start to think? Well, I don't know how Can I afford this? What can I do? I don't know. Let's go. And.

Tyson Gaylord [00:09:55]:

But your brain's on a mission, right? It's going to start going, looking around. It's going to start seeing things, start seeing opportunities. You're starting windows open. You know, a lot of times, opportunities, they're not loud and in your face, right? They're whispering. But if you're not tuned in, if you're not listening for those whispers because your brain's not tuned in to how can I afford this? How can I want a Ferrari? Okay, that's great. It's 1800amonth. How can I afford 1800amonth? Car payment. I need something bringing in that money, supplementing that money.

Tyson Gaylord [00:10:19]:

I need to make sure I buy right. Right. It's all these different things. You gotta. You gotta learn these different things, right? The cash flow quadrant. Understanding this was a key difference. Where are you? It's not necessarily one of these is bad or, or not, right? Cody Sanchez, you know, we'll probably get to her again. She has a little bit different take on this.

Tyson Gaylord [00:10:37]:

Equally, equally important, where are you? Where do you want to move? Conscious decisions, choices. Not what you're told, not what somebody else set out to you, maybe even a meaningful, loving family member or spouse or whatever has told you. You belong here. You belong in this quadrant, right? Understanding where you are and where you want to go, up to you. But you have to. You have to know where you're starting. Right? You got to understand. How do I build a proper foundation? Starts there.

Tyson Gaylord [00:11:06]:

And one of the. I think maybe the best inventions that came from this book is the cash flow board game. I have the physical copy at the time. I don't know what it costs now. It was $200. It was in his investment, but it's just a regular like Monopoly game. And the point of that was it's $200 because you are making a financial commitment to change your life, right? And this board game, if you haven't played it, there is an online version. I'm sure there's still groups and meetups of people that play this.

Tyson Gaylord [00:11:37]:

And a lot of times these guys are just playing business, right? They have grand ideas, but they never execute. But that's okay. What I found this game does is it reveals to you your true investor style, the way you spend and save money. It reveals this, right? And personally, I will mortgage everything I have. I will borrow every dollar I can when I find an opportunity. Right? That's my style. I played with my son at time. This recording he's 15.

Tyson Gaylord [00:12:08]:

We've been playing off and on for many years since, you know, he was a little younger. And he's got a little bit less of an aggressive style, but not very conservative of style. He, he, he, he will aggressively leverage things to, to buy good opportunities, but he also, you know, will pay down his monthly expenses versus me. I don't see the value, right? And so in the game, I'm talking about the game here, but this, this goes into real life, right? So this is kind of the point of the game. It shows you. Incoming balance sheet shows you this financial statement so you can learn different things, right? So on, on the game you, you know, choose a character and you have different expenses, right? I don't. And, and then the, the rate of money, the way, you know, the rate to borrow money versus the return. A lot of times to me I think it's like $10 for your hundred dollars or something like that or whatever.

Tyson Gaylord [00:13:06]:

If I'm gonna pay off something that's costing me $30 a month, that's $300 to me versus my borrowing power. So, you know, I think about those things a little differently. Some things are not worth paying off to me. When you pay off your things or you accumulate enough assets, then you get out of the rat race and you get onto this different thing and that's kind of how you win the game. My son's got a little bit, kind of a hybrid approach and I've seen people very, very conservative, very risk averse and this translates into their real life. So I think this is a great way to test where you're at. And a lot of times it'll show you where you're at mentally, but there's something a block in your real life. So I noticed that with myself, right? In the game I'm, I'm Free Willy, but in my real life I'm a little bit more conservative.

Tyson Gaylord [00:13:52]:

I'm worried about a little bit more about cash on hand, but in the game I'm not. So I try to bridge the gap between those two. I encourage you guys to check that game. I will link to the game in whatever formats I, I can find. I do know there is a digital version. I do think the hard board game, the physical board game, I believe it's a lot cheaper now, but I'll link to that if you're interested in. I recommend that if anything, go look for meetups and stuff in your area. I'm almost guaranteeing there still is.

Tyson Gaylord [00:14:18]:

And then financial literacy, right? This is the, to me, the Most important thing I learned here, I learned these terms, right? I learned these things. That is a lot of people's problems, especially with financial industry, right? It's terms, right? And you'll see this. We can argue and we can debate if this is on purpose or not. You'll see this in the medical industry. So this is an illegal industry. You'll see this in the financial. There's terms that are hard to understand. They're ambiguous or they sound crazy, and they really don't mean nothing.

Tyson Gaylord [00:14:47]:

They're easy to understand, but you need to be willing, you need to be unscared, you need to be whatever it is, not intimidated by these things and at least have a cursory knowledge of these words. So when people talk to me, you're talking to a financial planner, you're talking to a lawyer or whatever, you kind of understand what they're talking about, right? I'm not saying you need to be an expert, per se, but you need to understand what the expert is telling you so you can understand instead of just nodding along. I don't know what my doctor's talking about. He says something about cardiovascular apoe4. I don't know what he's saying. He's just throwing out different things, and I don't know what he's talking about. The lawyer was telling me about standing, and I. I wasn't standing.

Tyson Gaylord [00:15:24]:

I was sitting in the channel. And what they're talking. You need to understand these basic terms, right? And that's something. This book at least gives you a base knowledge, right? So the six core lessons in the book here, the foundational system rests on six primary lessons designed to break conventional employee conditioning. Readers routinely internalize the first two lessons while completely ignoring the operational demands of the subsequent four. The rich do not work for money. I'm sure a lot of you have heard this. There's tons of criticism around this, right? The rich, they'll.

Tyson Gaylord [00:16:01]:

They'll borrow against their stock. A lot of people complain about this, and Elon Musk and Bill Gates and all these type of people, right? Because they don't understand, right? And that's. Again, we can debate this. It's part of the system. It's part of the reason we need the tax base, right? We need the useful idiots. We need these people just doing regular stuff, not evaluating their life, not making conscious decision choices. And that's what my point in the show is, is I want just this information to you so you can choose, keep going the same way you're going. That's cool.

Tyson Gaylord [00:16:28]:

As long as you chose that. That's what I'm about, right? So wealthy individuals. So the risk. The rich do not work for money. Wealthy individuals acquire assets that generate passive income. You know, passive income doesn't mean you do nothing. Sometimes. Sometimes you can get to that point.

Tyson Gaylord [00:16:44]:

That's a separate topic. This removes the direct correlation between physical labor and financial earnings, right? I'm sure a lot of us have heard this. I make money while I sleep, right? These are different vehicles, right? I hired, you know, Tom, he runs that company. It throws off $35,000 a year. That comes back to me in dividends. I'm not physically there, but I got all that running. I got all these things going, right? That's forms of passive income, right? You talk about, you know, Bill Gates, you know, he built up Microsoft. Now he's not there anymore, but it still throws him cash, right? Elon, he built a Tesla.

Tyson Gaylord [00:17:14]:

He's not necessarily there, throws off cash. There's tons of examples of this, right? You know, but this is what the thing this is if you want to get to this point, there's lots of different vehicles to start generating passive income, especially in this digital age, especially with AI. And there's different things, there's lots of different ways to generate this, to become an intellectual capitalist, to monetize your knowledge and experience. And the more I think AI gets in and in different things, the human touch, the human experience is going to become more valuable. So can you come up with a course? Can you come up with a, A, a cheat sheet, a guide to passing tests or to, to doing these certifications that you wake up in the morning and 17 people that you don't know, never heard of or never will meet bought your course or bought your guide or bought your ebook or whatever it is, right? Signed up for your school, community, whatever it is. These are forms of passive income. It's expanding your mind. I'm giving you things here to go, think about later.

Tyson Gaylord [00:18:11]:

Make conscious choices. And then number two, the importance of financial literacy. The absolute amount of capital generated is irrelevant compared to the capital retained, right? Doesn't matter how much money you make, it matters on how much money you keep. So in the game, this is very, you know, evident. A lot of the lesser paid players, the janitors and I think it's a Garfman, different things like that. It's easier to win the game from those positions because you don't have a lot of expenses versus the doctors and the lawyers. It's. Even though you're, you're making a lot more Money because expenses are so high, it's hard to win the game.

Tyson Gaylord [00:18:51]:

And this is a game, the same game in life. Tony Robbins got a great book, same kind of concept. It's the game of money. It's a game. You got to understand how to play it. And it's. It's not a finite game. It's an infinite game.

Tyson Gaylord [00:19:03]:

It goes on forever. There's not necessarily a finish line. So you got to understand how this works. And then the specific license requires the ability to read and manage income statements and balance sheets, which is very well highlighted in the cash flow quadrant in the cash flow game. Understanding how this works, understanding how to do this. A lot of us, maybe we outsource this to software or we don't even look at. A lot of people don't look at their credit card statements. I don't understand that.

Tyson Gaylord [00:19:28]:

I don't want things charged, you know, but there's services that are built all around this. Right? Rocket Money is built on. I don't know what I'm doing. I don't. I don't know how many times I'm subscribed to four different DoorDash accounts and seven different Netflix accounts. How that happens, I don't understand. But there's industries built around your unwillingness to learn, your unwillingness to do the scary things, your unwillingness to do the hard things. Right.

Tyson Gaylord [00:19:51]:

Our choice is easy life, easy choices, hard life. What are you going to choose? I don't care what you choose. I just want you to choose. Okay? And then probably one of my favorite lessons, mind your own business. You can think of that how you want. And you're probably right. But in the text of this book is individuals must build an asset column independently of their primary employment. Right? What is the traditional things we hear about, you know, your 401ks, your pensions, and different things like that, Right? Whatever your choice is, that's fine as long as you're making a choice.

Tyson Gaylord [00:20:29]:

The text advocates for keeping a day job while simultaneously building a separate business structure. This is one of the things I fully didn't grasp. Right. I was under the impression that you can just do real estate things, don't need a paycheck very hard. You don't have money to get a mortgage. But this goes back to my thing. My limitation was I refused to get over. I chose the easy route and I had to make, you know, choices because I didn't fully understand the lesson here.

Tyson Gaylord [00:21:02]:

I didn't build a business. I didn't build careers. I just was like, I just got to Figure out the real estate part. That's all I need, right? So but keep worry about yourself, worry about your business, worry about your situation. So if you're not taking care of yourself, nothing, you can't take care of nothing else, nobody else, right? You got to start with yourself. You gotta individual must build an asset column independent of their primary employment. And this also makes you uncounselable, right? Buck you money or whatever. When you have outside things, you're not dependent on the economy necessarily.

Tyson Gaylord [00:21:41]:

You're not dependent on my employer's going to lay us off, whatever, right. You've got a little bit more bit of safety and structure now this maybe start out very, very small and then you can build over time and then the history of taxes and corporations. The wealthy utilize corporate structures to, to pay expenses first using pre tax dollars, right? That's a term maybe we, a lot of us don't aren't familiar with. They only pay taxes on the remaining net income versus employees pay taxes immediately upon earning our wages. That's what we see when we have a regular paycheck. We, you know, we go work at Uncle Sam's car wash and we have, we made a thousand bucks. And you see, you know all these things, Social Security, you know, FIFA, whatever, all these, I forget it's been a while since I had one of these, right? But you see all these things and then you got 727, you're like who took all my money? Right? Versus if, if you had a side hustle, you had your own business, whatever it is, you get a thousand bucks and here's your thousand bucks. Now you still owe the feds but you can lower your tax liability by buying things.

Tyson Gaylord [00:22:50]:

You, you know a good analogy. A friend of mine said it was everything's 30% off if you can think about like that, right? So you want to buy a new laptop. My brother just got a new company truck, right? So many different things. You're paying for these with pre tax money. So you know, see find a professional that, that knows how to do this stuff. There's a lot of people out there, especially on Instagram TikTok that are just donkeys going to tell you dumb shit. But find trusted people that then trust them. Verify, you know, trust but verify, right? And start finding out what does the government incentivize? That's what taxes are, right? The government says we need these things done and we're going to incentivize you with tax breaks to go do them.

Tyson Gaylord [00:23:37]:

We need housing, we're going to give you A tax break. We need data centers. We're going to give you a tax break. We need, you know, natural gas, we need oil. We're going to tax break There, there, there's tons of things out there. If you go look at the tax code, which sounds crazy, but there's, there's different sources and different things. You can, you can go and like I said, trust but verify. Don't listen to these, don't in it that tells you you can buy Louis Vuitton bags and it's a business expense.

Tyson Gaylord [00:24:01]:

It's not okay, you got to understand these things. But when you're buying things with pre tax money, right? Your tax bill can go to zero, right? And you don't, you're not worried about refund versus think about, you know, if you work a regular job, think about what happens, right? You get taxed and you get your money, right? Then you take that money that you got and you go buy other things and those things are taxed as well, right? Versus if you just had some sort of money from a different source, if not all of it, you get your money first, you go buy all your different things and then those are taxed and at the end if there's you know, a difference, you pay the little bit. If there's not a difference, maybe you get some back, maybe you pay zero, whatever. There's tons of different scenarios. But just understanding that there's possibilities, right? I never knew there was a pre tax thing. And the funny thing is my family owned businesses, but they never talked about these things, right? So I didn't learn these things from people that were actually running the businesses. And then five. The rich invent money.

Tyson Gaylord [00:25:03]:

Wealth is generated by recognizing opportunities that others miss and assembling the necessary capital and operational pieces to capitalize on them. So this is the thing too. A lot of us don't understand where money comes from. Money is invented. It comes out of thin air. When you take out a loan. We invent the money. Nobody had it, we invented it, right? The, you know, the bank.

Tyson Gaylord [00:25:26]:

Say the bank has a thousand dollars. Depends on the laws at the time of the regulation. At the time right now I believe it's still zero. So the bank has to have zero percent, but they can loan out the whole thousand dollars, right? A lot of times it's 10%, right? So the bank has a thousand bucks they can loan out, they have to keep 10% of that. So they keep 100 bucks and they can loan out $900, right? And when they do that, they're just Inventing money out of thin air, right? Credit card. Think about a credit card, right? Where did this money come. It just is invented alone. It's just invented money, right? So when you understand that, then you, you can understand that you can find resources and places where you can just get money out of thin air, basically, right? But you need to know where to deploy these things.

Tyson Gaylord [00:26:13]:

You got, like I said earlier, right? You gotta, you gotta listen for the whispers of opportunities. There's a once in a lifetime opportunity available every day. You just got to know where to find it. And when you tune yourself into these things, you'll start to see these things, right? Like classic example, when you're, you just buy a new car, you're looking for a new car, right? You're like, I want to get that new Tahoe. And all of a sudden you start seeing Tahoes everywhere. They're always there. But because now your brain is tuned, right? Your reticular activating activated system, something along those lines, it starts to. Your brain has a focus as a job, as a goal.

Tyson Gaylord [00:26:49]:

I'm suddenly looking for Tahoes. And you're going to find them. Now if you train your brain on. I'm looking for situations to deploy capital, whether it's my capital or I'm going to invent this capital, you're going to start seeing these things all over the place, okay? And then the final thing here is work to learn, not to earn. Employment should be used primarily to acquire new operational skills rather rather than for the sole purpose of a weekly paycheck. Now, I understand sometimes you gotta just have a job or you have a job because you just need the money. You don't care about it. Now twofold, maybe three.

Tyson Gaylord [00:27:32]:

Find another job that you enjoy. Or you can learn something from me. Get paid in the ojt, right? On the job training. Go get paid a job in an industry or a sector or in some type of adjacentness to what you really want to be doing. Maybe I can go work at Coca Cola and they're going to teach me how to drive big rigs. They're going to pay for it. I don't know what this I'm making up, right? Because I want to, I want to get my own trucking thing. I want to have like two or three.

Tyson Gaylord [00:27:57]:

Me and my cousin and my brother, we're going to all have our own trucks and we're going to just haul, you know, independent things and we're going to do our own thing. But I need to figure this out. I need to learn how this. So I'm gonna go work at Coca Cola. I don't care about Coca Cola, but I care about driving this truck. How do I start learning, right? How do they do this, how they schedule, how do they manage these things, how do they keep things coordinated, right? That's that ojt, that's learning on the job, you know, so there's lots of different things you can do. Maybe you pick up something on the side and that's where you're going to learn, right? A lot of things, a lot of problems, a lot of these different things is because we are not getting experience. You're gonna fail, you're gonna lose some money.

Tyson Gaylord [00:28:36]:

Make sure you can afford to lose it. You're gonna lose some time, whatever it is. But that's where you learn, right? We gotta get in, in the field, we gotta get in the game. If we're not in the game, we can read all the books, we can watch all the YouTube videos, we can have all the courses. But if you're never in the game, you don't know what it feels like to get hit, right? So do this on another somebody else's dime when and where you can. All right? And then the 10 steps to awaken financial genius. So beyond the six core lessons, the system outlines a highly specific 10 step process for activating financial intelligence. These steps serve as the behavioral protocols for the entire wealth accumulation system.

Tyson Gaylord [00:29:15]:

Readers to buy properties, skip these psychological prerequisites entirely. I am numero uno gold medalist in this category, so the steps here, I'm just going to shoot through them real quick. Step 1. Find a reason greater than reality. Establish a psychological anchor and a clear list of desires to overcome inevitable obstacles and maintain strict discipline. This is I, this is one for a reason, right? When you don't have a clear why, the smallest obstacle comes along, you're done. Okay, Step two. Make daily choices.

Tyson Gaylord [00:29:52]:

Continuously choose to allocate time and capital toward financial education and asset acquisition every single day. And if you tell me you don't have time, go look at your screen time and you can take off 30 minutes from that, you can take over an hour from that. Okay, you can find little snack pieces here and there. If you got to carry a book around with you, you got podcasts, you got audiobook, there's so many things, right? Instead of jamming out to the oldies in your truck while you're driving to work, throw on an audiobook, throw on a podcast about whatever it is you're doing, right? One percent better every day. That should be the goal three, choose friends carefully. You've heard this from here, you've probably heard this a million times. Other people, you're the five people you're spending most time with. And all these different, you know, attitudes around this, right? Leverage the power of association.

Tyson Gaylord [00:30:37]:

When you get around people doing things, you're going to start doing things. You want to get in shape, get around guys that are working out, you want to eat better, get around people that are working out, you want to buy houses, get around people, buy house. You want to buy a car, whatever it is, right? You're going to pick up things from them. Just being around them. You're going to learn, you're going to start, you, you're going to find opportunities. People are going to like, hey, what's up? You hang around a lot? Well, you know, I got five grand. I want to kind of get into the car game, but I don't know, they're like, oh, let's jump in on a deal and oh, okay, well, whatever, right? You're going to learn. Surround yourself with individuals.

Tyson Gaylord [00:31:08]:

Consistently discuss wealth and operational opportunities. This is a good one too. I heard a guy, I don't know him, but let's just. I, I know of him. Whatever. I know, I know him from podcasts, I know from the Internet. Okay. Sometimes nowadays it feels like, you know, these guys, he used to go sit in a wealthy neighborhood in coffee shop type scenarios and just listen to the conversations around him.

Tyson Gaylord [00:31:31]:

Surprise what people talk about in public. But you're listening, right? You think, write things down. What does that work? What does that mean? Let's talk about diversification. Let's talk about underwriting. What's it talking about? Leverage buyout. What are you talking about? Write these things down. Oh, look it up. Oh, okay, that's interesting.

Tyson Gaylord [00:31:47]:

I kind of like that idea. That's something I could be interested in, right? You know, being lucky. You know, interject yourself in a conversation, mind a very polite, non rude, non way and say, like, hey, listen, you know, outcomes come across, shop at time. I'm working, I come in here. I hear you guys a lot. You know, I got a couple questions about this leveraged bio thing you're talking about. I'm interested in this thing and it sounds whatever, right? Maybe, I don't know. Just saying.

Tyson Gaylord [00:32:09]:

Okay, step four, Master formula for rapid learning. Master one specific wealth bidding strategy. Thoroughly, thoroughly one, thoroughly before moving to the next. This is all of my habit all the time, right? I got 10 things going at the same time. I like it like that. I know it's wrong as mosey. If you're familiar with him, he'll tell you to start to write when you're not focusing on one thing. If you think you can multitask full of.

Tyson Gaylord [00:32:35]:

None of us can think, we can feel like we can. You're diverting attention. My brain does this and I gotta refocus myself. One thing. I'm working on one thing right now. And you develop. Instead of developing mastery, maybe these are skills you can do, you can sell, right? Boom. Another business.

Tyson Gaylord [00:32:53]:

I don't know, this one is probably one of the tougher ones. Number six, pay yourself first. Exercise supreme self discipline. Allocate capital to investments before paying any external liabilities or creditors. Okay, maybe not invest before you pay things. You can get in trouble. Not saying that, but what's the thought here, right? Pay yourself first. I want, this is, I want you to this concept, right? When you get paid, what do you do? Check comes in, I owe the gas company, electric company, rent the car, paying the car, I've got 800 bucks left.

Tyson Gaylord [00:33:33]:

Or what this is advocating for in so many terms is I get paid automatically. Whatever, 10, 20%. A dollar ten a fucking penny goes automatically to a savings account. I automatically, I stick it in a jar in my house. I don't care what it is. I. It's the habit I want you to develop. It's the, it's this mechanism because if you don't do this, you're like, oh, when I get money, I'm gonna do it.

Tyson Gaylord [00:33:58]:

No, you're not. You don't do it now. So a lot of times it's very easy. You got your checking, savings, you know, whatever, or an investing account, whatever it be, right? First item, after the feds take their cash, you throw some to you, right? So you got a thousand bucks. Let's just go 10%. Let's throw a hundred dollars. You don't see it automatically. Make it automatic.

Tyson Gaylord [00:34:20]:

So it's easy because you're not going to do it. Things gonna throw it to the, to the savings. Throw it to a money market, whatever you want to do. Throw it in the freaking jar. Don't care what you do, just do it right. And then you got 900 bucks to pay your stuff. I'm not an advocate for cutting stuff out, but maybe at first you got to cut a couple things a little less. The coffee shop, I don't know.

Tyson Gaylord [00:34:42]:

Those things are kind of dumb. I just say make more money. It's faster, it's easier. Maybe pick up extra shifts somewhere. Pick up a doordash and pick up an Uber one an hour to whatever it is, make up that difference, right? These are expanding the mind. We're thinking, we're looking for ideas, we're trying to be creative. I don't want to hear I can't do this because of no wrong. You're not allowing yourself, your brain to find solutions, to find answers.

Tyson Gaylord [00:35:11]:

Okay, we talked about this earlier. Don't limit yourself. Whatever you think, you're correct. So make sure you think about the right stuff. Okay? Step six. Pay brokers. Well, it's an interesting concept, right? Compensate professional advisors generously. High quality advice generates exponential financial returns.

Tyson Gaylord [00:35:30]:

You know, kind of, I guess think about this like the bartender, right? You're, you're, you're, you know, typical bartender, good manage drinks, they, they get a little saucy, right? Same concept, right? When you, when you're starting nickel and diming. These people like everybody is maybe they're like man icing is always good to me. I got this killer deal, nobody knows about it yet. I'm gonna give him first crack at this and I don't even need a big commission. So many things happen. People are generous. There's a rule of reciprocity. When you're generous to people, people go either way to repay you, even if it's exponentially more than you gave them, right? Also it's a good thing to do.

Tyson Gaylord [00:36:11]:

So there's that as well. So practice this, right? Pay a little bit more because it's going to save you in the long run. Get a better tax person, get a better whatever it is, you know, financial advisor, shoot mechanics. I mean so many things in life, right? We do this for we cheap out and it winds up costing us more in the long run. So let's, let's go that step seven. This is an interesting one. Being Indian giver. Focus heavily on the rapid return of initial capital to achieve a zero cost basis on all investments.

Tyson Gaylord [00:36:45]:

So now what this is about is, you know, this is a kind of classic example. So we'll go ahead and buy a house, one hundred thousand and eighty thousand dollar mortgage. We'll go in there, we'll fix things up, we'll get it rented. Not a house is worth 150. So what you'll do, go, give me an example. You go to the bank, reappraise the house, that's worth 150. You only got an $8,000 mortgage. So you go ahead and you refi, you take the 150, you keep, you keep your change.

Tyson Gaylord [00:37:09]:

They give the 80, you got the Rest. They call this infinite returns. So now you have no more money in there, and you got eight. You know, you got 70,000 bucks left over or whatever. And you go into this again. This is the concept, okay? You'll hear this in stock investing as well, too. You know, you get to a certain level, I'm gonna. I'm gonna peel off some of this, and, you know, I put a thousand dollars into this stock.

Tyson Gaylord [00:37:35]:

It's up 3,000. I'm gonna take my thousand back. I got 2,000. I'm playing with house money now. I'm good. So these are things to think about. Use assets to buy liabilities. Delay gratification entirely.

Tyson Gaylord [00:37:50]:

And I know this is difficult, especially this day and age where you see it on the gram, you're like, I get the Lambo, it's gonna cost me, but I'm gonna look good, right? No. Delay gratification, right? Hard choices, easy life. Easy choices, hard life. Use passive cash flow generated by assets to fund lifestyle upgrades instead of earned income. This thing you should be doing whatever you want. Have fun, whatever you're into, I don't care what it is. And when you can have assets, pay for liabilities. Life is fun, right? You're not stressed about anything.

Tyson Gaylord [00:38:26]:

You know, it's going to be great. I want a Ferrari. I got stuff pays $1800 a month. I don't care, right? See the difference? You know, I like. I like Rolexes. I like Richard Mills. You know, I like Patek Philippe's. I got money coming in.

Tyson Gaylord [00:38:41]:

I don't care how much it's. Not to mention you buy, right? You understand what you're doing. Those things also can become assets, right? So use that instead of. Instead of. I'm a. I'm. You know, I'm gonna. I'm gonna spend it before I get it.

Tyson Gaylord [00:38:57]:

I have a half out of that, too. I know the money's coming. I'm gonna spend it right before I get it. But we need to understand these things, right? Understand where you're at, how to make changes. Step 9. Choose heroes. Utilize the power of myth, the behaviors and operational mindsets of highly successful investors. You can get these virtual mentors in whichever way.

Tyson Gaylord [00:39:17]:

A lot of times, AI can have fun with these things. You can consume them from books and podcasts and old, maybe interviews or whatever it is. Find people that you want to be like. Take different pieces from people's lives. You want to be like, don't idolize these people because you don't know their real life is like. You only know what the part of their life you see that you like, right? They could be horrible parents, they could be horrible fathers and husbands and whatever. So make sure you just take what you want. You know, I said a lot of times, AI, you can have these conversations with these people.

Tyson Gaylord [00:39:47]:

You know, you like, you like Mark Cuban. You can throw him in, AI, you can have a chat with him, the different services, you can have fun on all that books. Somebody spent hundreds, thousands, millions of dollars, years of experience to write this book for 29.95. All their information and all their life experiences in here. Use these guys as mentors too. Step 10 Teach and receive. Activate the power of giving. Share financial knowledge to reinforce personal learning and attract reciprocal value.

Tyson Gaylord [00:40:14]:

Right? I learned so much more about this because I needed to refresh myself and drill down and understand these concepts so I can explain them to you. If you've ever had a child, they ask you why 4,000 times and you understand it in your brain, but you can't explain it because you don't understand it enough, right? So now when you're teaching, you've got to get a deeper understanding to share this with others, right? And what is the best part of this? Your friends are leveling up. Your family is leveling up. Your neighbors are leveling up, right? You all can have fun together. That's the fun part about it. Even strangers, you'll get great messages from people you never heard, never meet, that says, thank you very much teaching me now. My life is better because of this. That freaking awesome.

Tyson Gaylord [00:41:09]:

All right, the cash flow quadrant dynamics. Like I said, we did episode nine and 10. It was a long time ago, information is still the same. And we had a fascinating conversation real quick. It's just a framework. It's left side of the quadrant represents active income, being an employee versus self employed or a specialist, like a doctor, a lawyer, different things like that, Right. B is a business owner. This side is, you know, more of the passive kind of side.

Tyson Gaylord [00:41:40]:

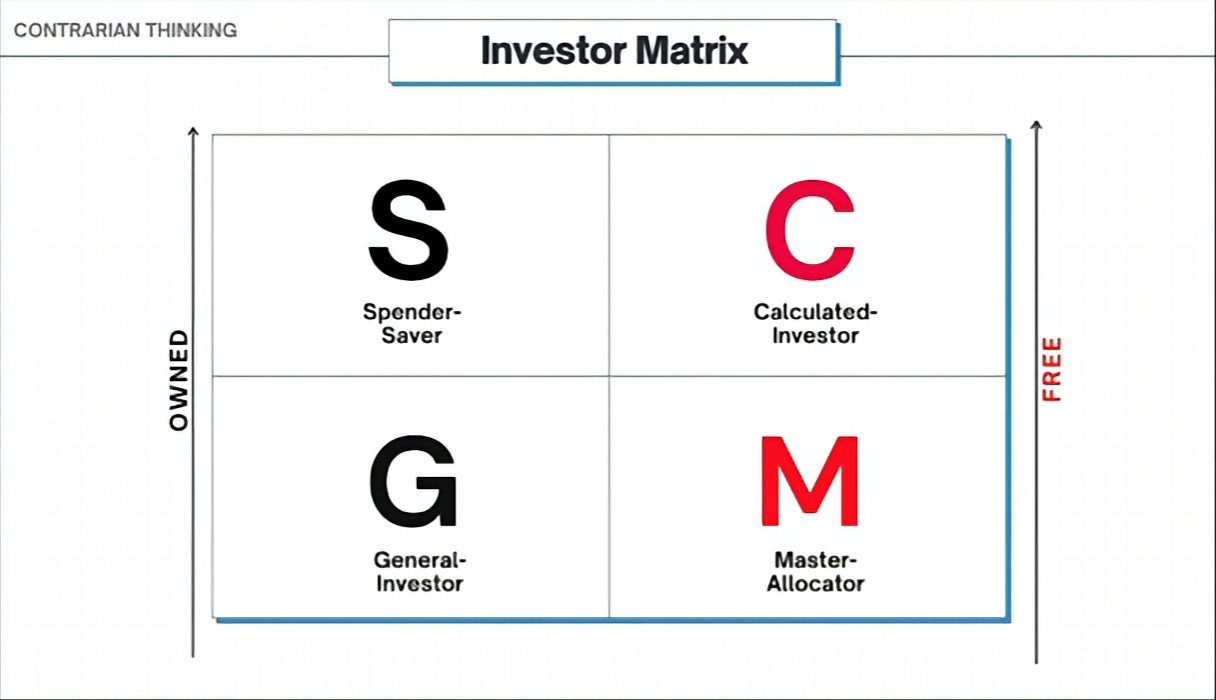

And then investor, this is. These are the two areas where the theory, the idea is money works for you. If you ever heard of Shartank air, watch Cameron Leary. He talks about his dollars, his soldiers, he sends his soldiers out and they should come home with more captured dollars. But if it helps you visualize this process, this is kind of the thing. We get into this more in the episode now. Something I came across kind of maybe, maybe three, four months ago, which kind of maybe got me down about thinking about doing this was Cody Sanchez. She's great.

Tyson Gaylord [00:42:14]:

She'll get you into this. B and I side as well. She's got different tactics, different strategies. Like I said, looking for ideas, folks. We're looking for ideas. We're looking at the things that get our blood pumping. We're like, yes, I'm excited to get up today because I'm gonna go do whatever. I'm gonna go fill up all my vending machines and this is great.

Tyson Gaylord [00:42:37]:

I spend an hour a day and I make $12,000 a month. I fill up 1700 vending machines and it's so much fun and I love it. Whatever. I don't care what it is. Right. Figure out you. She's great. She has a different take on this.

Tyson Gaylord [00:42:54]:

I'll link to the YouTube video where she goes over this in the show notes too. I'll have a little street gap screen grab screen shot of Robert Kiyosaki's custom project of hers. You can see the difference of two. I'd say they're basically the same, just a little bit different. Thinking of beverage but rich dad, poor dad lied to you by Cody Sanchez. I'll link to that. See her perspective. Maybe, maybe it clicks with you.

Tyson Gaylord [00:43:18]:

That's what, that's what I'm looking for here. Right. A lot of times we hear the same thing from, from Coach A and Coach B, but Coach B, the way they said it better, the analogies or the delivery style, whatever, it clicks with you. That's all I want. I want this information to click with you. And then I'm gonna get here to the seven steps to the financial fast track. The system provides another specific sequence designed to a transition an individual from an employee to an investor. This sequence detail in the cash flow quadrant follow up material outlines seven concrete investor phases.

Tyson Gaylord [00:43:50]:

Mind your own business. We talked about take control of your cash flow. This is where the individual must sit down and map out a comprehensive plan to minimize debts and eliminate liabilities. Right. So when you don't have credit card debt, student loan, all these things holding you back from, you know, from these things, then you feel better, right? You feel lighter. You know, if you're sick, you're not like, I need to check. I worked with a guy, his entire month's paycheck was only his mortgage. And then during the financial crisis we started, you know, getting a little bit less hours and stuff like that or whatever.

Tyson Gaylord [00:44:25]:

He lost his mind. If we work 39 hours, he didn't have enough money to pay his mortgage. He had to dip into his, his wife's portion. So that is so much stress, right? Or it just. If, just right now you're in a shitty position. That's the thing, too. Mindset, right? Are you broke? Are you poor? Those are two. You think they're the same? They're not the same.

Tyson Gaylord [00:44:48]:

Poor, that's forever, right? Broke. It's temporary. Where are you? If you keep saying yourself is poor, guess what? You're correct. If you're like, my family was poor. We grew up that way, or whatever it is, I'm not. Remember these I am statements. I am not Right now. I'm a little cash jack.

Tyson Gaylord [00:45:08]:

I'm a little. I'm broke. You know, whatever temporary I am working out. I am going through these steps. I am doing these things because I am going to be better. I am going to get out of this situation. I am not gonna let three generations, four generations or whatever dictate what I am going to do with choices I make. Right? You need to start by controlling yourself.

Tyson Gaylord [00:45:28]:

If you got too many, what he calls it in the book, do that. Too much shit. All these nonsense things sitting in your garage, taking the money. Get on Facebook, Marketplace, whatever favorite place you like, get rid of that shit. It's just you're paying to store it. You're not using it. You paid to get it. Get some money back.

Tyson Gaylord [00:45:46]:

Eliminate. Minimize your debts. Okay? There's good debt, there's bad debt. We'll get into a little bit more later. Right? No difference between risk and risky. That's up to you. You decide what that means to you. True investors understand that investing is not risky if you are highly educated.

Tyson Gaylord [00:46:03]:

Right. It's not necessarily college. Right. You just got to understand these concepts and principles. Ignorance is what creates financial risk. Right? There's a great story. I like Richard Branson from the Virgin Group. Different.

Tyson Gaylord [00:46:15]:

Virgin Mobile. You know Virgin? He wants to start an airline. Crazy. Whatever. He's like, you're gonna have to have hundreds of millions of dollars by airplanes. He's like, why? I'm just gonna go to Boeing. You got a bunch of planes over there, right? Yeah. You don't use them, right? Yeah.

Tyson Gaylord [00:46:29]:

How about you let me borrow them for a little while? I just pay at least payments. If I don't, this doesn't work out. I'm just giving back to you. They're not doing anything anyway, right? That's not risky. What's his downside? He's capped his downside. Right? We got. This is the difference. When you.

Tyson Gaylord [00:46:43]:

When you have financial literacy, right? You understand the difference between risk and risky. Okay? Not betting the farm. You're not throwing. You're not taking a mortgage out Second mortgage on your house, and you're betting it all on, you know, dogecoin, whatever. That's dumb. That's risky, right? Unless you have some type of unfair advantage, okay, you understand these things, that's fine. But are you being risky risk, Are you on top trends, whatever. Got to have a natural intelligence.

Tyson Gaylord [00:47:09]:

Trust but verify, okay? Decide what kind of investor you want to be. The system categorizes investors into different levels of sophistication. The individual must actively choose what desired level of engagement. I had a conversation with somebody, the same thing about this, right? They're talking about, oh, I put money in this and I don't. I haven't seen any returns. Well, what are you optimizing for? What are you. What are you into? Why so much to learn? Well, that's your problem. An hour a night for a month, you'll be pretty educated on what's going on.

Tyson Gaylord [00:47:41]:

I met the episode on this, right? 17 minutes to be better than 95 of the world, that's all you need. So it's bullshit, right? It's laziness. It, you know, it's. Whatever. It's fear. It's. Whatever it is. Just start step one, whatever it be, okay? And then seek mentors, right? This will help.

Tyson Gaylord [00:47:58]:

See, people have already been where you want to go. Follow the yellow brick road, right? They've laid down track, get on it, you know, they've already made the mistakes. Start with their mistakes and you'll make your own. And you can lay it on track for the next guy because you. Okay, let's go make this appointment. Your strength, the individual must accept mistakes and learn to leverage failures as highly effective educational tools. There's this great book on this. I'll link to it.

Tyson Gaylord [00:48:29]:

Feel forward and a couple of different. You've got to embrace failure. This is one of the problems with school, right? We are. Whatever it's taught is hammered into us. No, you can't make mistakes. You can't do anything. No, you got to do it. That's because you're in the game.

Tyson Gaylord [00:48:41]:

If you're not in the game, you're not fumbling, right? You're not in the game. You're not missing a basket. You're not in the game. You're not taking a shot. You miss, you know, the puck ain't gonna go in if you're not there to kick it, whatever, right? This thing, you're gonna up Michael Jordan, whatever. Kobe Bryant, whatever. LeBron James missed 25 million shots. You don't remember those.

Tyson Gaylord [00:49:02]:

You remember the 17,000? They made and won the game, won this year, won the championship, whatever the field goal, that's what you remember because they were on the field and they were not afraid to kick that field goal. They were not afraid to throw the pass in the corner. They were not afraid to take the shot with the clock counting down right on the field in the game. You're gonna make mistakes. It's how you frame it. Everything how you frame it. What do you believe about yourself? Starts with belief. With belief.

Tyson Gaylord [00:49:31]:

Confidence. Confidence comes and goes. When you have the belief, you can regain the confidence to get back in the game. And the power of faith. The final step requires a deep belief in personal capability and a commitment to continuous forward momentum. Better believe. And then we have the premature real estate jump. Analyzing the operational failure.

Tyson Gaylord [00:49:51]:

The central thesis of the. Of this podcast review is. Is on the border, you know, the broader real estate education industry that was built upon gross misinterpretation of text. I was a victim number one because I limited myself in reading. That's my problem. It's all me. It took me a while to figure that out, okay? Readers of the book frequently absorb the motivational rhetoric regarding assets and liabilities that immediately attempt to purchase real estate. They skip the mandatory intermediate steps of financial literacy, corporate structuring and business development.

Tyson Gaylord [00:50:30]:

That was the thing. When I. That was the first. When I read. When I say, reread it. When I read this in the entirety, the first thing I said was, holy shit, I missed the most important step. Getting businesses and entities and different things bringing me money. I was too reliant on a job and saving my cash.

Tyson Gaylord [00:50:48]:

I was like, man, that's been my problem this whole time. And I didn't even realize it because I did not take the time to actually read this and actually understand material. I fell for the real estate convention education system hype, okay? That's what I'm trying to avoid here with you. And then we have the illusion of the investor quadrant, okay? The most profound operational affair comes from an employee. The E attempts to jump to the investor I quadrant using highly leveraged real estate. The systematic methodology dictates that true investors fund their acquisition using the surplus cash flow generated by a business. I would also say from self employment, from other investments, right? There's lots of things here, right? It's the excess cash flow. Another thing I missed another thing a lot of people miss because it's easy.

Tyson Gaylord [00:51:43]:

We get caught up in, in these, in these, these hype promotions, right? They. They feed on our primal instinct. They get into our Olympic brain And then to get us all going, right? And next thing you know, credit cards are flying and loan documents are being signed. That's one thing I remember. This one real estate one we went to, me and my buddy were all into this and they were like, go, go, go online. And this is right before like the 12th financial crisis. This one things are probably the craziest. They're like, go online, go to stanford.com, sign up for whatever, the cheapest, whatever, dumb basket weaving 101.

Tyson Gaylord [00:52:24]:

And then boom, as soon as you got your enrollment thing, take that, you go get a student loan for as much money as I'm telling you. They told me, I'm not, it's not financial advice. I'm just telling, right? Go get a student loan for the most money you can. Fuck the class because you only got it so you can get the student loan. I mean, I mean I tried because that's, I didn't know anybody. My financial intelligence was low. But all these, all these other things around that time, I was like, I'm not trying to get a morgue, I can't think. This is not real, right? And it wasn't.

Tyson Gaylord [00:52:54]:

But if you had a heartbeat, you could get a mortgage. And I was like, nah. But I'm glad I never, I never had double clock. I didn't get the financial. I'm glad I didn't get the student loan. You know, student loan money, not financial advice, please don't be dumb. But financial money, financial aid money was cheap and it kind of doesn't affect you if you're not paying it. It doesn't really affect your credit.

Tyson Gaylord [00:53:19]:

I have a friend that bought a house, a ton of student loan debt. They're like, they didn't care about my student loan debt. They just care about the other stuff. So essential also understand you can never get rid of student loan debt without paying it off. You can't file bankruptcy. I believe there's some instances when you die, your family still owns that student loan debt. I've heard of instances where your Social Security is being taxed because you still own student loan money. So please be careful.

Tyson Gaylord [00:53:42]:

Financial intelligence, right? This is what we need. Trust but verify, right? Okay. So this is, you know, go. If you're interested in financial quadrants and how we go and jump around, go listen to that episode. We'll get more into it. But when a standard employee takes on massive debt to acquire a rental property without the protective shell of a functioning business system, where that be or a high income job or something, you need that money, right? They're not acting as an investor, they're simply acting on a highly leveraged secondary job as a property manager. And a lot of times too, if you're not, please give financial and tax advice from a tax free. But the way I understand it is if you're not spending a certain amount of time and effort managing whether short term rentals or regular rentals, you don't get like the real estate tax status, something please go see a professional because you're working a cyber job.

Tyson Gaylord [00:54:36]:

Like there's no way you're working 16 hours. Like it's highly. IRS is like no, it's kind of not likely. So understand that, right? You know, if people are telling you oh you get this real estate tax exemption status but then you really go look into it, you gotta spend like 40 hours a week actively, you know, doing these things. You've gotta like have documentation and proof and all this stuff. But you're working a regular job because you're just glorified landlord. Be careful there, right? This is when proper advisors, they're proper mentors, proper people. Especially when you're looking for these tax professionals differently.

Tyson Gaylord [00:55:10]:

Ask them do you have experience in real estate or even find somebody that. I am a CPA that exclusively deals in short term rental property. I'm a exclusively deals in real estate. I, I only work with real estate professionals. I only work everyday investors like those guys are the greatest because they have a very deep understanding of, of the law. Not just the law, way the law is interpreted, the way the, the tax court rules. So they're going to say well yeah, that's what that says. And you May heard on TikTok there's a gray area but if you can look at tax square records they're like there's no gray area.

Tyson Gaylord [00:55:44]:

They're very clear on how they rule, right? Or you know, things change, right? You know the one time, you know, meal deductions were different and car travel was different and this, things change. You got to know somebody that's on top of the game. You'll find people when you start looking around just love this stuff. They love the taxes, they love the numbers. They're just so into it. This is, they're reading tax books and they're reading CPA stuff and they're taking some on the side because they love it so much. When you find those guys, they're going to help you keep and make so much more money and they're going to alleviate so much stress. But understand all that, right? This, it all comes down to this Right.

Tyson Gaylord [00:56:22]:

And then we have the abandoned abandonment of rigorous financial literacy. The author repeatedly emphasizes that financial literacy serves as the absolute foundation to all wealth. A true investor must know how to read an income statement, a balance sheet and a statement of cash flows. They must thoroughly understand the mathematical relationship between these documents to succeed. Understand there's a financial, you know, income statement, balance sheet, cash flow statement that the bank likes. Right. The bank likes seeing certain things. But what Mr.

Tyson Gaylord [00:57:00]:

Kiyosaki talks about, I call him Uncle Robert, Hawaii thing talks about something different. Right. The. The real stuff. Right. The, you know, it's like, oh, your house and all stuff. Okay, yeah, that's great. Put that down.

Tyson Gaylord [00:57:12]:

When you want to get homes and mortgages, whatever, that's what they want. And that's what's going to inflate your ability to borrow. Not give me financial advice, just telling you how things can and are. Whatever. Then, fine, do what you want to do. But in the reality of it, those things, you have to have a true financial outlook on yourself. Right. What is your true cash flow situation? Okay.

Tyson Gaylord [00:57:37]:

Understand those things. And then the misapplication of. Pay yourself first. Step five of the system. These are, I think these. We're into the criticisms now, I believe. Sorry about that. Step five of the system is to mandate to.

Tyson Gaylord [00:57:51]:

Is the mandate to pay yourself first. The book advocates for taking capital off the top of every paycheck to invest in assets immediately if this action leaves insufficient funds to pay creditors and monthly bills. The author suggests that in the pressure of the creditors, force the individual to create an incentive. Force the individual to create an incentive in an environment to create new income streams. Right. You're putting the pressure on. I don't think it's a good idea. But if this something you have thought about evaluating and said, listen, it's a killer opportunity.

Tyson Gaylord [00:58:27]:

Make shit up. I'm gonna pay my rent this month or my mortgage. I'm not gonna pay my car note, pay any of my bills. I'm gonna take all 35, 100 that I make this month and I'm gonna put it here. And I'm gonna suck for this month because it's a killer opportunity. I'll deal with the late fees and all that stuff. And I. This is something.

Tyson Gaylord [00:58:45]:

It's a calculated decision. Hey, do what you want to do. You're gonna though most of us, this is America or some type of free country, whatever the hell you want. But understand, I want you to make a conscious choice, not an emotional show. If this is emotional, go away. Somebody's pressuring you don't do the deal every single time. You'll hear this from tons of people where you're like, hey, man, come on, man, we need, we need the money tonight. We need the money by Friday.

Tyson Gaylord [00:59:16]:

It's gonna close. You're gonna miss out. Those types of deals are the ones that come back to bite you so hard. Run away, okay? If you're feeling emotional about this thing. Oh, man, Bitcoin is whatever. Damn, I'm gonna take, take the night off. Go away, Go on a walk. Take the emotions.

Tyson Gaylord [00:59:37]:

Bring those down, okay? Then rationally make a decision. Maybe find an AI, a friend, a spouse, whatever, a cousin, a brother, whatever sounding. But hey, listen, okay, this is gonna sound crazy, it must sound dumb, but that stress tests me. Pressure test this idea with me. Find out my holes are where. Where is my thinking going wrong. Am I being too emotional? Okay, I just want you to think. I want you to make conscious decisions, right? And the misunderstanding of leveraging debt.

Tyson Gaylord [01:00:06]:

The system clearly distinguishes between good debt and bad debt. Good debt is utilized to acquire assets that produce enough cash flow to cover the debt service while simultaneously generating a profit. Bad debt, let's think about credit cards and stuff like that, right? Is utilized to acquire consumer goods and depreciating liabilities. Once you understand the difference, you know, you know, Dave Ramsey and stuff like that, these guys talk about, probably the best advice for most people is don't get into debt. Don't do it. Especially until you understand how to use good debt to your advantage, okay? Start small. Start with something little, you know, maybe take out some type of margin on, on your stock portfolio or your crypto or something like that or whatever, right? You know, but understanding, right? So I'm gonna take, I'm gonna take $5,000 loan against my stock portfolio, right? And then I'm gonna go get something that is going to generate me $6,200 a month. I can pay back my, my loan payment, right? So you got to understand that, right? You gotta, you gotta have the financial intelligence.

Tyson Gaylord [01:01:19]:

And then here's some more somewhere, the dark side of the criticism, right? Addressing the valid criticism. I'm not, you know, I, I want to talk about all of this, okay? Because a lot of times these things get bad raps because whether it's financial professionals protecting their industry, that's a lot of times that's, that's what it is, you know, people misinterpreting things or, or taking things too literally or whatever. So the first thing here on my list is the, the fictional mentor, a Lot of people have. Have said that there is no rich dad. It's just a character. You know, through all these journalistic investigations. Who gives a. That's what I'm saying.

Tyson Gaylord [01:02:03]:

Who. What are you. You're just looking for something. Just look. You're just looking for something to, To. To criticize. It's fucking best. It's a.

Tyson Gaylord [01:02:13]:

It works as a fucking metaphor. Who cares? He's just giving you a story about. And I've heard. I'd say on decent authority that there is really a rich dad. But who gives a. It's just a story. It's just an analogy, right? This. This person from this background.

Tyson Gaylord [01:02:30]:

His, his poor dad, highly educated. I think he was like the lieutenant governor of Hawaii or something like that or whatever. School board, whatever. PhD, poor, broke all the time. His, his rich dad. I, I believe he didn't graduate high school. From my understanding, he. He developed a lot of Waikiki and stuff like that.

Tyson Gaylord [01:02:52]:

So that's what. That's what. At best, it's an analogy. It's a metaphor for, for two different. He. I think it's like I said, as Rich said, I believe he didn't finish high school or just high school or something like that. From, from the street school. The hard knocks.

Tyson Gaylord [01:03:05]:

Why aren't those valid lessons? Why aren't these two metaphors valid metaphors? Who cares if these people are real? Okay, this is what I'm saying. Stop listening to these freaking dumb people. Just take a second. Some first principle thinking. Break. Break this stuff down. Who gives a shit what. Okay, whatever.

Tyson Gaylord [01:03:23]:

Moving on. And then the dangerous and legal advice. There's stuff. Maybe an original book that's outdated. I don't. I'm sure that in this new book, this 20th anniversary edition, I'm sure there's outdated stuff. You know, there's a lot of criticism. They call it the terrible tactical advice in the book.

Tyson Gaylord [01:03:43]:

The text casually recommends trading on non public inside information with friends, which is a federal crime. And unless you're a senator, whatever. And poly markets is a thing now be careful with that. It's also suggests highly questionable tax strategies. Go see a professional that knows for reals. It's not hard. What are we complaining about? Right? And then write off personifications and stuff like that. Go see a tax professional.

Tyson Gaylord [01:04:09]:

They'll tell you what is and what is not. It's not hard to meet requirements or not meet requirements. Don't do stupid shit. So, I mean, these are fair criticisms, but you're just looking for problems. You're being maybe too Literal, maybe it's outdated information. Don't be stupid. Don't be a useful idiot. Go find professionals that know what they're talking about and they have skin in the game, right? That's the thing.

Tyson Gaylord [01:04:33]:

When these professionals have skin in the game, there's a whole lot different. When I can just. I talk shit to you. I'll tell you all stuff because it doesn't matter. It doesn't hurt my pocketbook in any which way. I'm gonna say something different in general than somebody that, that I don't get paid if you don't succeed or I don't make money if you don't make money. You know, I, I'm on the hook for your, your tax preparation, whatever it is. You know, Find people that have some type of skin in the game, right? And then garbage investment vehicles.

Tyson Gaylord [01:05:04]:

Again, this is lack of imagination, right? Lack of nuance maybe, but lack of people's personal preferences, Right? So the book dismisses reliable index funds. He's just not into the stock market stuff. Whatever. Do that if you want. And actively promotes highly speculative high failure vehicles like penny stocks, IPOs and multi level marketing. Are there not people that have made a good living if not wealthy from these things? Of course. If that's not your thing, don't do it. If you look into you like, ah, don't do it.

Tyson Gaylord [01:05:40]:

Okay. Valid criticisms, but on first thought, it's like, who gives a. Okay, this should go for lots of things in life, right? When you hear this shit, who gives a shit? I don't care, you know? And then we have operational oversimplification and lack of mechanisms. A persistent complaint among professionals is that the book is devoid of actual concrete financial mechanics. Relies heavily on emotional platitudes and motivational rhetoric. Yeah, there is, but again, use your brain trust, but verify. Go find people, go find these things. Go investigate these things.

Tyson Gaylord [01:06:21]:

The broad advice to simply buy assets is. The conception is conceptually sound. Yeah. Okay. The text completely fails to explain how to properly value an asset, how to secure substantial financing, how to underwrite a commercial property, or how to manage systematic risk. Because that's your job, okay? You need to go out there and figure out what you're into. Are you into vintage plates? Why is he gonna say that in the book? That's your thing. It's to get ideas, to get your mind flowing, to get your brain engaged.

Tyson Gaylord [01:06:58]:

Okay? And then unfortunately, we had the Predatory Aftermath seminar. Industry and people that prayed on the knowledge gap. They explained the book that tells you to invest, which is I, you know, Felt fell victim to. I hate that, but I feel prey to whatever. That's my fault. And then with the upsell funnel, right, this massive gap, you know, this seminar is free, but if you want to know real information, you got to come to this next one next weekend, and that's 300. And then when you get to that one, it's like, here's a little bit of something. But if you really, really want to learn how to do it, you got to come to the next one.

Tyson Gaylord [01:07:33]:

That's $30,000. And that's when you really, really learn. You got all these people that are going to help you out. Unfortunately, there was a lot of. And you know, there's people that made money, and there's probably just as many people that are still paying off that debt. But again, trust will verify. I don't see a lot of this anymore, but please don't, don't fall victim to this. There's shit I see on Instagram, TikTok, whatever, you know, YouTube, like just, you know, if it sounds too good to be true kind of thing, like, these things are cliches because they're true to them.

Tyson Gaylord [01:08:03]:

So just be careful, right? And then this is how we're going to end this. We're always going to end this with solutions. That's. That's how my brain works, okay? The legendary takeaway attracting the true value separate mindset from mechanics. I want to conclude by telling you guys how I like to use the book today. It's cognitive framing. It will successfully change how you view your paycheck, your house and your debts. The traditional narrative dictates that security is found exclusively in a college degree salary job and a primary residence.

Tyson Gaylord [01:08:42]:

And in 2026, we know those things were kind of never true, but a lot of us grew up on, you got to go to college or you're a fucking loser. You'll never make any money. You're going to be this. We've heard all the things like a college graduate makes a million dollars more in your life now, whatever, okay, if that's your thing, because you want to be a doctor, a lawyer, an engineer, go do it. There's also a lot of jobs that can make equally, if not more money without going to school, going to a trade, going to an apprenticeship program. There's. So it's about choosing what you want to do, what you find interesting. Okay.

Tyson Gaylord [01:09:20]: