Time Is On Your Side

Retirement Savings

What does saving $100 a month towards retirement really added up to in 30 years?

Is time on my side?

Does compound interest really make me that much money?

We answer all these questions, plus other scenarios in the realm of retirement savings. This is an interactive episode where we run a bunch of situations in a spreadsheet to see what things would look like in 5, 10, 20, even 40 years in the future.

Books & Links From The Episode

Favorite Podcast On This Subject

Books

More books in past episodes on the money subject.

55: Book Review: The Richest Man in Babylon

The Richest Man in Babylon Subscribe to our YouTube Channel George Samuel Clason American Author George Samuel Clason was an American author. He is most associated with his book The Richest Man in Babylon which was first published in 1926. […]

42: Movie Review: Generation Freedom

Movie Review Generation: Subscribe to our YouTube Channel About The Docuseries “I’m wasting my life pursuing a living. I battle non-stop emails, unnecessary meetings, overbearing coworkers, and a company that doesn’t care about me. I know I’ll be ordering off […]

37: What You Should Know About… Your Money

Your Money In this final episode in our series ‘What You Should Know About…’ the most requested topic, YOUR MONEY! We give you ideas and insight on Automagic Budgeting, Investment Ideas, and your money mindset. This is an introduction to […]

28: Understanding Credit

Understanding Credit Credit can be confusing, slow going and hard to get right. Having good credit can save you tens of thousands of dollars over your lifetime and give you access to opportunities for a better financial future. We want […]

17| Who’s Got My Money?

Who’s Got My Money? Understanding Banks and Making Your Cash Work for You Welcome to another episode of the Social Chameleon Show, where our mission is to help you learn, grow, and transform into the person you want to become. […]

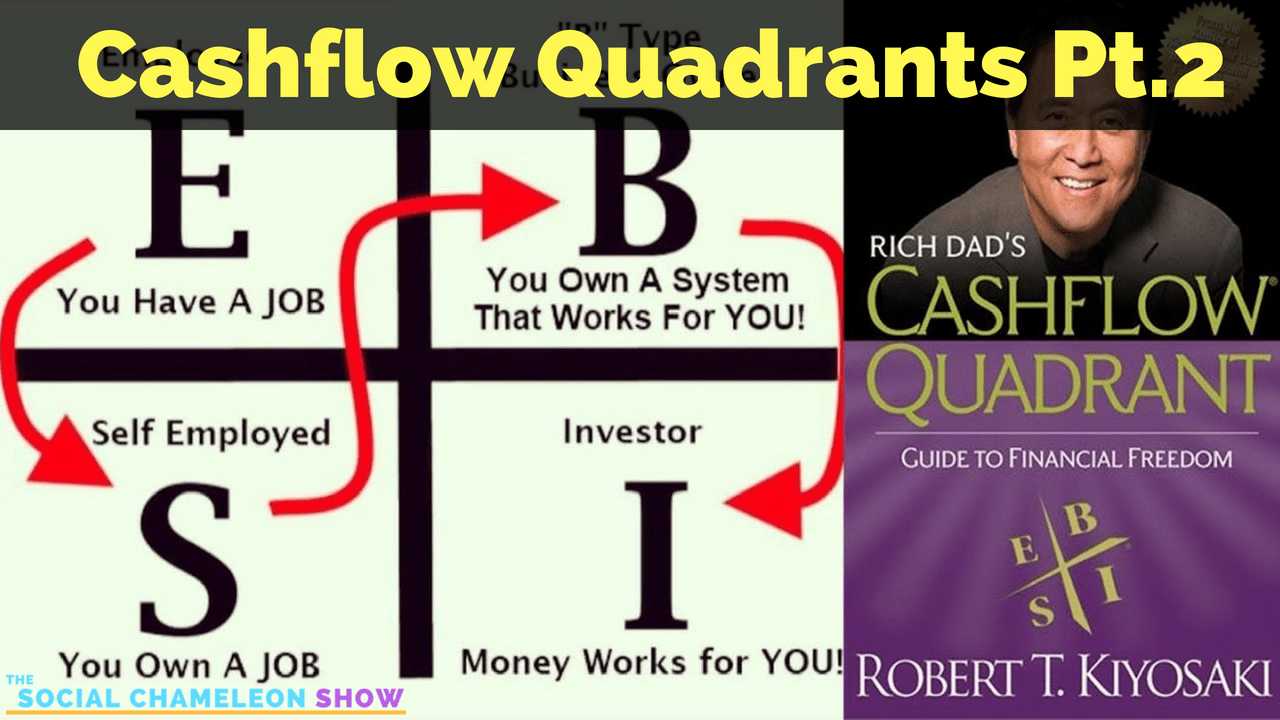

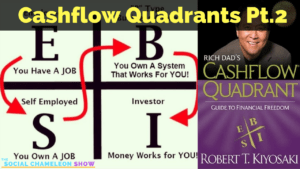

10: B & I Cashflow Quadrants PT 2

Cashflow Quadrants | Pt. 2 This week we continue our special 2 part series on Income Sources know as Cashflow Quadrants. This week we move over to the Right side know as the B (Big Business) & I (Investor) Side. […]

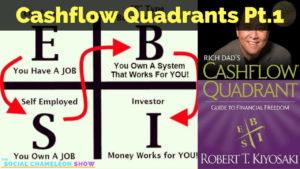

9: E & S Cashflow Quadrants PT 1

The Social Chameleon Show This week we have a special 2 part series on Income Sources know as Cashflow Quadrants. On part 1 we talk about the Left side know as the E (Employee) & S (Self-employed or Small business) […]

Episode Transcriptions

Episode Transcriptions Unedited, AI Auto-Generated.

Speaker 1: 00:15 Opening Music

Speaker 2: 00:15 Welcome to the social community show where it's all grow up. You learn, grow, transform, what you want to become. Say you were talking about retirement, retirement savings for one k, whatever, anything in those lines. Saving for, for different things. We don't want to kind of walk through some different models. We'll do our best to talk through it. If you're interested in seeing what we're doing, please head over to youtube and you can watch the video. We'll be sharing the screen and going through an excel document, giving, throwing some different scenarios out there for your people to think about. It's really, this is what this is about. This is information. It's entertainment. We're not trying to give you s or solicited financial advice. We're not financial people, planners, whatever. Here's some things to think about. I know personally, you know, I, I never, I never got started and it's so late in life and we're going to kind of walk through with them one of those scenarios where maybe, you know, you're, you're in your thirties or you know, close to your forties like I am and you didn't really start well. See where you're going to wind up. Maybe you're close to retirement, maybe five or 10 years out. We'll kind of give you what that could look like. If you only got that short timeframe, which you can kind of maybe, maybe expect traditionally or historically with different types of returns.

Speaker 3: 01:25 Yeah, definitely. I guess I was just brainstorming one night, I'm like, you know, we talk about all these, I guess investment ideas, investment opportunities. Some of the stuff we talk about is, I guess aggressive into business things. Sorry, I'm gonna Sneeze there, but I'm a aggressive into, you know, making businesses and all that kind of stuff. And I was thinking, you know, what about the average person who doesn't really want to start a business, they make enough money at their regular job and they just want to start putting money away for retirement. So that's kind of the model. Again, this is set in that model and like you said, we're not, you know, financial planners or anything, but hypothetically speaking, if you wanted to do this this is just another tool that you can use to at least create your plan. You know, you'll have to formulate and recheck every year to see if your parent is on track. And we'll also put this spreadsheet out and the examples that we have out so that you can use this on your own. Again, if you're the scenes who on a podcast, you can check it out and it's also can be not show, click on the shoulder links and, and download it for your own personal use if you want to. That is our gift to you. Awesome. So dizzy. Yeah. And

Speaker 2: 02:43 You can just, it's just an excel, excel file, Google sheets. You guys easily plug in different options, different scenarios. Could they change things and see how they play out over, I think we have it set out for what, 30 years, 40 years, something like that.

Speaker 3: 02:57 26, I guess to be,

Speaker 4: 02:59 And then you can just, if you want more, you can pull it out and make more so easily adjustable for you guys.

Speaker 3: 03:07 Yeah. But anyway, enough about the technicality though. For those of you that are with us on the podcast a, sorry, it's a more of a visual effect on the ceasing, but we will go ahead and describe everything that we're trying to do this on here, that way everybody can kind of follow along. And so this is a little spreadsheet that we have. So I have labeled it in the back. It's just I IRA ETF worksheet. For those of you that haven't followed us before or heard about it some of the more literature nowadays, mutual funds are getting rather expensive, rather pricey on their fees. So there are other things that you could put out there. So just as a little reminder, I put ETF and IRA can easily be a mutual fund or whatever type of investment vehicle you want to use. And from here, the first sheet, what do we have here? Is this 10, 10% max? Is that

Speaker 4: 04:07 Right? That's why we're going off. I guess that's the historical average or returns you can expect in these types of funds. You can also change this percentage to maybe you've got a high yield savings account or I a checking account. You can see what you can expect if you were to leave money in there at 2.5% or something like that and see what that would look like as well. You can easily change the interest rate to match whatever source you're using for this model.

Speaker 3: 04:33 Yeah, definitely. And so this model was just created, hypothetically speaking. So we have the year here on the far left column starting with 2020 as this airs, it will be 2019. So you know, this is actually genuine. If you want it to use this right now, you could, you can just put year 2019 in there or before you even try it. Maybe you can practice this year, putting that money away or whatever the case might be. Just practice saving and then that way you can implement this first of the year. But you know, don't let that allow you to procrastinate. If you can start doing it now, do it now. And this is only includes your contribution to your 401k for three B, whatever you have. If your employer matches that, then you basically just kind of add that to your contribution, you know, or is there just self employed?

Speaker 3: 05:27 Maybe you can put your own contribution and then also as your own employer you can contribute as well. Some of the we're look into. Yeah, definitely. So this is just in general, we're just gonna keep it as simple as possible. If you are a bit tech savvy and you know how to manipulate this worksheet go ahead and play with it and have a blast. I have a ball, the split, you know, definitely like to bring awareness to things and if you know how to take this idea and go with it, then go right ahead. So anyway, I'm going down further in the sheet. So 2020 is the starting date. We are going to have a starting balance of absolutely zero. And from there I said Max contribution, but I think next year the Max contribution will actually be $19,500. But currently now in today's year 2019, the Max contribution that you can actually put in there is 19,000. Again, see professional advice, they may give you other numbers other than that, especially if you're in the later years and you have the ketchup provision and all different depending on what type of account you have. But anyway, I digress. So for this, so starting at 2020 with 19 and again, we're going with the 10% rate of return. If you think that's ridiculous and you can't get that, then okay. Put a realistic number that you think you can do. You can change that number to anything you want. But anyway,

Speaker 2: 06:57 Yeah, we'll go, we'll play with these a little bit and a few minutes and show you some different scenarios if you want to do

Speaker 3: 07:04 Right. So, you know, at 10% you put in 19,000, you just moved to zero over. So you're gonna get $1,900. And that's your game. And then from there you have your original sum of 19,000 so at the end of 2020, you will have the total value of $20,900 Yay. Hey, we got where we, we're growing in there making money. And then from there again, the next year you're going to start with 20,900 bucks. You're going to contribute another 19. It just gives you the total of 3,990 then from there you're going to get 10% return, which is 3,990 bucks. Then you're gonna put all that together and then you'll have a grand total of your second year of 43,890 bucks. So you know, as you can see, the gains on this aren't really too amazing. The first two years. But I guess what number, do you want to jump ahead or you want to keep going or you just want to jump to your five maybe?

Speaker 2: 08:11 Yeah, he told, Yeah. So yeah, we can just kind of get people to say, if you kept doing that 19,000 nothing changed. Everything averaged the same. So you're five, you'd look, you'd be up to 161,000 and some change and in 10 years from there you'd be close to 400 grand and so on. And then we go down another, you know, by 2040 you would be looking at just under 1.2 million.

Speaker 3: 08:36 Nice.

Speaker 2: 08:37 So you can see how every, you know, every soften and starts at doubling and on. So think about this now. Yes, these are spectacular late night TV, commercial returns. But guess what? You did nothing. You didn't do any extra work. You didn't have to do any extra things. You just took the money you already are earning and put it to work for you. So think about it that way, you know? Yes, you could probably make better returns if you do other things. But this avenue, you're not doing anything. The money's out there in the world. It's working for you. You're not doing nothing but you already are normally doing. So take that into mind. And then, so at the end of our model goes down the 26 years, you'd be sitting on 2.5 million plus. But I mean just,

Speaker 3: 09:19 But look at that though. You go from the, you know, at the 40 year mark, you're at 1.2 million.

Speaker 2: 09:27 Yeah. So 20 years from now you'd be sitting at 1.7 but six years later, yeah, your money has doubled. You double. Yeah. You know what I'm saying? Like that,

Speaker 3: 09:39 You know, that's, that's the thing that I kind of wanted to talk about this episode is like not very many people understand that. And that's kind of why I went slow when I was describing the first two years of this process. It's like you put 19 away, you get 20,000 and some change and you put another 19 away, you give 40,000 and some change. You know, for most people they're like, what's the point of that? You know? But then, you know, when you start getting down to, like you said, the 10 year marker and you're looking at 1.2 million. Oh, that's great. Like, that's, that's something if I can do that for 20 years. Yeah. But you know, the next six years after that 20 years, that sort of magic happens. Yeah. That sort of big stuff starts happening. You know what I mean? That's where you get those exponential returns. If you're putting in 19,000 but you're pumping out millions, like yes, I, I don't know. Okay.

Speaker 2: 10:35 Yeah. To do another four or five years and you're talking another few million dollars does doubled up on top of itself.

Speaker 3: 10:42 Right. And the, you know, I mean, this is just hypothetically speaking, wanted to, I guess take this contribution and a, again, this is just these numbers, I guess what we want me to just do, we have examples, we have some example sheets that we can play with. Okay. So yeah. So for those of you that are watching on the youtube thing, at the bottom, there's, I'm just hitting examples so that we can kind of just learn how to work through this. For those of you that are listening to the auto, sorry, that doesn't really apply to you. But anyway, so I'm going to take these numbers here. Now, for those of you that don't know how to do excel, you can kind of just watch me do this, but basically you highlight, pull this little square and they'll put those numbers down. Then, you know, quit Joel CEO, all of these shortcuts and this. But you know, if you don't know how to use excel to worry about it, it's nothing. You know, we're not doing anything that's unheard of here. But anyway, so

Speaker 2: 11:42 That's great tutorials online. You can get any help. Don't hesitate to reach out. I can point you in some directions to help you guys. Okay, so we're going out from

Speaker 3: 11:54 Another four years is that we're doing

Speaker 2: 11:56 The four years.

Speaker 3: 11:57 Okay. So yeah, another four years to 2050 right. And going to put this out and sorry to add these up and then we'll know. Exactly.

Speaker 2: 12:10 So you only went for a 2.5 million to just under 3.4. Just a minute. 3.5 million.

Speaker 3: 12:17 Well, no, it's 3.8 whenever you're looking at,

Speaker 2: 12:20 Well, oh yeah. I'm sorry. If you're letting me, yeah, so you, you, you've done a little, a little over double, I'm sorry. Yeah, 3.8 million. Right? So you move from two five to three eight.

Speaker 3: 12:30 That's awesome. And that's in four years, you know, so that, you know, and again, the, see these are astronomical numbers. I understand nobody needs $3 million in their retirement account. I don't necessarily,

Speaker 2: 12:45 I disagree. You never know what the happened. And that money's nice when we get older and you know, there's a lot of health problems pop up and things maybe you know, you want to do, you're not going to be earning any money. So you gonna be living on this for, especially as we get older, you know let's say you retire at 65, the average person lifts at least 80 and you need 20 years of money. I'm saying you're not getting any pensions or anything like that, which is very likely nowadays, no, people aren't getting pensions. There may or may not be social security or maybe a small thing. You know, you'd be living on this 3.8 million for the next 20, 30, 40. I mean, do you live to a hundred, which is, which is likely. And especially as we get more technology, that's a very likely thing that can happen. You're gonna if you don't want to go back to work and you don't want to be doing other income generating things, you're going to want such a nice nest egg. So you don't have to worry about paying your bills when you're doing your open, when you're old. That's really not something that's gonna be fun.

Speaker 3: 13:39 Right. And so for those of you that are wondering, maybe some of you out there are watching this and you are close to retirement and you're kind of thinking about, well you know, 3 million sounds great, but I don't know if I really need that. There was a study out there I think called the trinity study. So what people are doing nowadays is you take this total number that you will owe gross or accumulate in your working years. I kind of don't want to use the three main cause that's just retarded. Let's go with the the the one that's just under 1.2. So this is again, if you put 19,000 away for 20 years, you'd have just under 1.2. So you, you take that 1.2 I messed that up. But anyway, see if we can do that. And then oh yeah, put the value the time [inaudible] I won't happen there. Just you can just type it in or whatever. So anyway, 1.2 and then from there you take that number and you take 4% of it. Okay. So at a withdrawal rate of 4%, which means you take 4% of what's left in there or just 4% of that number and you withdraw that amount like that. This is what you're going to be able to make every year. So this will be, yes.

Speaker 4: 15:11 So a good way to kind of work up to the number you're going to need is if you start with what your, your current living expenses are. Like, say I need 50 grand a year to live, you can take that number and know if I have, I only need 50 grand a year at a three or 4% withdrawal rate, how much money will I need to accumulate to still live at that lifestyle? That's a good way. So at the end in mind, and then you work your way up to the ultimate number you're going to need. So whatever that comes out too for you.

Speaker 5: 15:43 [Inaudible]

Speaker 3: 15:45 Downstairs, dude, I didn't, but anyway, she says it's a little bit different than excel, but ah, yeah, it's, it's all right. See me

Speaker 4: 15:57 K 20 k 21

Speaker 3: 15:59 Oh, is that what it is, Keith? 21 yeah, I know. Anyway, so for those of you that are out there, okay, so I slide my little sheet over here. So if you have that 1.2 and you are at the 4% withdrawal rate, which 4% of 1.2 million for those of you that are good at math, it comes out to $47,881 alright, so that is hypothetically speaking in the year, starting next year with nothing in your retirement, you put 19 away grows at 10% equals 1.2 but what that actually equals is for the next 30 years, you'll be able to take out just under $50,000 a year, right? And that's only from this retirement account. That's not including social security or any other additional things that are going to be put in there. So you can kind of take that number and do that number with whatever you want. Right? So you want to continue on, right? Like we said to 2046 which is where this number originally started. You have 2.5 now, so we'll just put that in there. So two, 2 million, 500,000 k 4% and of course this didn't change.

Speaker 4: 17:20 You're using, you're using the h cell. That's why so use the case l

Speaker 5: 17:25 And Monday, right?

Speaker 4: 17:29 Yeah, yeah, yeah,

Speaker 3: 17:30 Yes. For those 11. So sorry. So if you take that and that comes out to that 100,000

Speaker 4: 17:38 Underground a year. Yeah.

Speaker 3: 17:40 Yeah. So yeah. So I mean you, you see the difference between, you know, what is going on and this is all gonna work.

Speaker 4: 17:52 You know what? So some people are saying 3% can we see what 3% looks like a real quick. Sure.

Speaker 3: 17:56 You can see or what do you want to do? 3% of the 1.2

Speaker 4: 18:00 Never seen another withdrawal as a redraw rate of 3% instead of 4% withdrawal. Yeah. I mean, whatever number is going to be comfortable for you. There you go. 75,002

Speaker 3: 18:08 And a half. It's 75 and then if you want 1 million, 200,000 and you're looking, okay.

Speaker 4: 18:18 You did, cause you went from the h cell. But yeah, this is the fun about doing this live.

Speaker 3: 18:26 Yeah, but it's here now. K 21 times. Oh, I just says that cause I can't, I'm going to move my box here. It's just the value is greater than actual box in Schiller's

Speaker 1: 18:43 [Inaudible]

Speaker 4: 18:45 Is it techs and can't be quarterly turn number. Oh, I think the way you wrote it. Oh, I need to add an extra zero. Yeah. Okay. So three to six miles.

Speaker 1: 18:54 Okay.

Speaker 4: 18:54 All right. So if you, if your lifestyle is a comfortable $36,000 a year, then you would know. Now you need 1.2 million. So you can live that way for the next, in theory, 30 years at that constant withdrawal rate of 36,000 and I think the three equations,

Speaker 3: 19:12 Yeah, three or 3% is kind of the conservative approach. A lot of people still use 4%. So you know, this is just how these accounts work. You have to keep in mind that yes, while you're growing the account, you're going to put all the money into stuff and making it grow at 10% and this is the part where you should lead with your financial planner to talk about. But once you have that money accumulated, you may not want to put all of that into growing investments, right? Because if it goes away, hang on, we're using 10% as an average because there are some years that you need to make more than 10% but there may be some years that you actually lose money. So I mean, you just gotta kind of keep in mind that, you know, you got to put stuff out there in order for it to grow. If you don't put your soldiers out there to work, you're not going to grow. But at the same time, some your soldiers die. So,

Speaker 4: 20:10 And I think this is a good thing too, it's so hard for us as humans to think this far in the future, 2030 40 50 years. Like what am I gonna need? So, but if you looked at this and said, I, I, we, you know, I make, we make 36,000 a year. That's where we, we, maybe that's not what you make, but that's what you guys use and that's what you live on. And you can go and say, okay, we're going to need 1.2 million and as the years go on and things will up and down, up and down it, you'll have less anxiety about this because you're like, listen, I know it's 10 15 2030 years from now and then we're going to 1.2 I know there's gonna be ups and downs, but we already know we've done the math that eventually when we get to our target goal date, as long as we have that 1.2 or more, we're set and you can kinda help with the anxiety of this, the, the, the ebbs and flows of the stock market and of life and things and say, it's okay, things are up now.

Speaker 4: 21:00 That's fine. These are down now. That's fun. But we know where we're headed. We know we're going to get to this 1.2 and I think you can think a lot of stress off yourself and you can start to visualize. It's a lot better.

Speaker 3: 21:10 Yeah. And just kind of understand that, you know, this is, this is just hypothetically speaking, like, you know, it's always good to plan for things. I like planning for things and this is just one way that you can plan and get out there. Like I said, we're going to make this sheet available and if you're listening to this, like think about it, like how much money do you make now here, you know, when you retire, don't you want to live the same lifestyle if not better? Yeah. Or maybe you have a higher paying job. Now let's just say you make 100,000 a year, but you only need $36,000 a year to live. Like great. You can start using this model is a perfect model for you. In fact, you're probably not ideal for three B, but she started out higher on top of that and put money into that and have that grow at 10% like you opened up a lot of options.

Speaker 4: 22:05 Yeah. So with that, let's, let's say, let's say you're asking, you know what this is, this is my mom and I use it. When I get to 1.2 I'm going to stop contributing. What would that look like going forward in this model? So at this year, mark zero out the contribution from then on.

Speaker 3: 22:20 Right? And that's, that's the other beauty of it too, right? When you, if you know what that number is, it's like, Dang man, I've been putting, I've been putting 19,000 away for 20 years. Like I've been, I've been scrunching now I'm going to live the good life. Right? So zero this out and see what your, you would still even see a grand total in your face. Yeah. So this is going 2040 ones. There's 2015 let's make that work on region zero. Yeah, zero all the way down to zero and then go on [inaudible]. So this will take us out to 2050 yeah, we'll still in

Speaker 4: 23:00 In 2050 if you are not taking money Alesis let's just hypothetically say I'm as soon as your portfolio hits that 1.2 is your goal. From then on you stop contributing until you hit retirement, which isn't gonna be in 2050 you will still have a total of, what is it looking like?

Speaker 3: 23:15 But just under 3.5 million. Yeah, but see, but see, that's crazy. You know what I mean? And that's the, that's the other beauty of it. It's like you put money upfront and like the end result is not that much different. You know, it's like you've got to do the work upfront and maybe there's some millennials out here that you know, you're like, oh, you know, I don't want to put 19,000 or whatever you want to put away for 40 years. Okay. Then don't let this, how about let's, let's see what 10 years

Speaker 4: 23:46 Looks like at 19,000 what does that look like? I was going to say five. Okay. You see five? Yeah. Let's, let's go from, so 2025 is your last contribution year. So if in 26 down we're going to go to zero.

Speaker 3: 23:59 The way this is done is, you know, so we're actually, you don't want to contribute. We're going to put 19 in [inaudible] in in 2019 is one, two, three, four. What does that look like? Five years to me. But anyway.

Speaker 4: 24:14 Okay, okay, let's, let's do 20 from 2012 from December 31st, 2025 you just stopped. No more contributions for effort.

Speaker 3: 24:23 What are we looking at? So if you just did that for the first five years on the right. Yep. And in 2050 you'd have 1.7 million,

Speaker 4: 24:32 Right? You could expect to have somewhere around almost 1.75 mill, which still puts you above your target goal in this scenario of 1.2 million.

Speaker 3: 24:42 Exactly. But you know, this is for people that have that time, right know. So if you're starting in your mid twenties and you're like, okay, what should I do? How should I invest? Most people think about buying a house first and it's like, okay, you're going to save this money, you're going to put it down on a house. And that's good. I'm not saying that that's a bad idea. I used to sell real estate once upon a time. I still do every now and then, but this is another consideration.

Speaker 4: 25:09 Yeah. I mean even, you know, even if you had only five years to go, you could expect somewhere around 160 grand at just five years of quick contributions. Say you're 16 you're like, damn, I fucked up and I need to catch up. Here we go. You can expect to have 160 k waiting for you. In theory, if everything, every year averages like we have it, that's not so bad either. That's gonna really change a lot of people's things new. That is the difference between you work in another three years instead of five years or you know, or, or, or pulling from here instead of there or leaning on your kids or something to, to do things for you.

Speaker 3: 25:48 Yeah. And you know, again, this is, that's why we want to go ahead and grab this worksheet, put it out there for you to play with and use. But what about those people out there that, you know, they don't make $19,000 a year.

Speaker 4: 26:00 Oh, you're right. I don't have 19 grand to put away. It's a mass contribution. What is that? A month?

Speaker 3: 26:06 That a month is a little over 1500. Okay. 1500 away every month. That'll be 18,000.

Speaker 4: 26:14 Okay. So yeah, so you know, rents, I can do a hundred bucks a month.

Speaker 3: 26:20 Okay. All right, so 100 bucks a month. So we're talking about 1200 a year.

Speaker 4: 26:26 Let's see, let's see, what, what does that look like? I'm, I'm fresh out in our first out of college, mass of my first job. That's all I can do right now. I got, I gotta get my student loans paid off. I want to also say for a house. Okay.

Speaker 3: 26:39 So again, see this is the model you only to put a hundred bucks in a month and that's fine. $1,200 a year. And again, this is just for five years, assuming that it grows, you invest everything and it grows at 10% you know, let's just say, let's, let's talk to real people. Here you are 25 right? This is a real scenario, 25 job. You know what I mean? You put money in from, you know, year 2022 year 25 yeah. And then by year 2050 was 25 years later, it's like the 110 grand and you only put in what, six years? I mean, granted, something like that, but that's still something, you know, it's not as, it's not as astronomical as $1 million, but you know what I mean? Like what again, this is $1,200 like you can continue to do this throughout your entire life. Pretty sure.

Speaker 3: 27:40 How about this? How about the first fibers in my life? I Max out at 19 what did I, what we did and we ended up, we, yeah, we didn't you, you ended up with like 1.7 million. Oh yeah. Okay. Yeah. Right, right. So there you go. You did the first five years, you're like, you can just do that. Right? But I mean, this example further, right? We, we, we already know that you have to keep contributing and that he know the gains don't really pick up until about 20 years later that year from 20 to like 25 years. You know, that's when you start getting the exponential growth. But if you can put away $100 a month at 25 you should be able to continue to put $100 a month out. In this week, I got a little bit more raise. I'll do one 50 a month now from here.

Speaker 3: 28:30 From 25 years. Yeah. But the ones that are already a month a year, so let me see that. So a one 50 times 12 months, oh, excuse me, hit the wrong button here. So $150 a month times 12 months, we're looking at 1800 bucks a year. Let's do that for the next five years. So we did the first five, we contributed 1200 bucks. Next five years, we're gonna contribute $1,800. So all of 20 2032 we're looking, okay, so you're like, you say that. Yeah. So now we're looking at the end of the 2050 you're gonna have about 200 grand, but you see what I mean? Like that's where we already know that like, you know, and this is kind of the things that you can work on is like start small with a a hundred and then keep going. Right? yes. And you can do this.

Speaker 3: 29:20 You can play this game at home with yourself and say, okay, you know what? And then from third, from, you know, for the next five years after that, I can do $200 now. Yeah. So the next thing I'm playing with that. Yeah. And then, yeah, so you can just kind of go in here, grab this, and then just take it down. You know, here we go. And then look, you know, you said you're getting closer, but let's just say you wanted to do 200 bucks a month or the rest of the life falling away. Okay. Now what I'm saying? Like it's just, it's out there. It's like, yeah, 330,000 like you just, it, it takes $200 a month, make $300,000 I took, I do all day or week. That's it. It's crazy. Like, and how exponential that is. Sure. You're going to do the 4% that's may not be enough.

Speaker 3: 30:11 But one of the thing is that you're, you're starting it, you know, this is money. You know, this model is designed to be an IRA account or whatever the case might be, where you can't touch the money without penalty, but there are certain things you can do. Like I know for a fact you can grab some of that 300,000 and take it out and uses a down payment for your house and then from there, pay that money back to your, to your IRA to give whatever kind of percent return you want. You loan it to yourself and then now you know you're going to get 4% on the money that you loan on top of the 10%. You know what I mean? Like you just kinda gotta think about things and how it's going to go. But just understanding that if you start small, you know, and like there's instead of like, yeah, you, you can only put 100 bucks a month now, but as you get older, as you make more money, you can put more and can treatment and,

Speaker 4: 31:08 And that's something you want to think about every, every few months, every year or something. When things happen, when you get a raise, like, okay, I got a 3% raise, I'm going to take one and a half percent extra, I'm gonna put that into my thing. Different scenarios like this, you're going to start to get paying off and say, you know, I paid off my student loans, took me three years now guess what, instead of 1200 you know, you're studying your four, I guess what? I got this extra $300 a month student loan payment. I don't have to make any more. So now I got 400 bucks extra a month. I can put it towards this. You can start and then, you know, as things go on in life, you start constantly reevaluating constantly. You know, if you know your target is, if you know your targets is 1.2 million, you've got to figure out what do I need to do to get enough money coming into this scenario every, every month. And you start playing with it. You can start changing numbers every, you know, two, three years up in, you're a little bit more helping in finding out when you to get to your target number, you know, and then you can start making those adjustments.

Speaker 3: 32:04 Yeah. And then another thing you can add on this is like, just keep in mind, you know, for millennials out there like this is 2050 is only 30 years. Yeah, you can, you can keep doing this all the way down to your 40 you know, what a, where, whatever the case is going to be. It's like going to go 40 years. That'll take you, you know, to 2060 and basically you just grab all of these columns. Sorry, I believe this one whole row and just drag it down. Yeah. And then we'll, we'll do all of those and then just slowly but surely. But keep in mind that if you're a millennial, yeah, a hundred bucks a month, in 30 years, I'm going to have 300,000 right. But you have a lot more time than I do. Right. You know, it's like times on your side and let's just kind of drag this out for 40 years and let's see what you come up with. Right. So basically 100 bucks a month for the first five years, the next five years, you change it to one 50 a month. Right. And then after that, and then you don't touch it, and we'll just slowly [inaudible] all these columns down here on then Oh yeah. You could've helped somebody.

Speaker 4: 33:16 I didn't, I didn't know I could have, I didn't think about it. Yeah, you're, look, you're just, you're creeping up on 1 million bucks.

Speaker 3: 33:22 Right. And this is $200 a month, you know,

Speaker 4: 33:27 $20 a month for how many years is that from 2032 to 2060 you're just doing 200 bucks a month. Steady every month for just under 30 years.

Speaker 3: 33:38 You know? And then you know, and that's not including, if you would've started from 200 bucks in your 25 right? So you know, just keep that in mind. It's like, yeah, this 1.2 million seems like something that's unreachable. It's like re if you're 25 right now and you got a decent paying job and your mate, let's just say you're 25 now, you make $36,000 a year. You can put some of that money away. Like that's not even 10% of your income, right? We talked about this in richest man of Babylon, right? One 10th of your income should go back to pay yourself.

Speaker 4: 34:13 So do that. Start, start that. Let's see the 3,600 right from the top, 3,600 and just just right all the way down, 37 bucks. You just do, you forget about it. You set it, you forget it, and you never go, go back and change it. You just always doing that temp, that initial 10%

Speaker 3: 34:32 And this comes out again to a whopping $300 a month people.

Speaker 4: 34:37 So run that down for the whole column for 36 years, 30 40 years.

Speaker 3: 34:43 Okay.

Speaker 4: 34:44 You have two Nino. Yep. Your initial 10% I'm sure you got raises over the time and things have changed over the years, but you're over your 1.2 million out target now.

Speaker 3: 34:56 And again, it's, this is just, this is all simple math, right? Very, very simple math. So just picture this. If this is you listening to this video, you're 25 years old, you make $36,000 a year. You're sitting here thinking, you know what? I don't really have, I don't really know what's gonna happen in life and I don't know how to make $1 million. It's that easy. Yup. Put 10% of it away. And with that 10% put it into some type of account that's gonna grow 10% and just continue to do that for 40 years. Yup.

Speaker 4: 35:34 No. Imagine if you're constantly updating this and adjusting when things happen,

Speaker 2: 35:38 This numbers are going to start to get bigger and bigger and bigger. In three years, you get a raise, now you're making 42,000 so now your number changes and another in five years you get a promotion. Now you're making 96,000 and these numbers start to grow, 10% grows. This is going to start to explode like we've seen earlier, and we started getting onto Max contribution level,

Speaker 3: 35:58 Right? Maybe we're talking about the Max contribution, but if you noticed, right, when we, when we did the first one, you have to Max contribute for five years, right? We did it. You put 19,000 in. That's comes out to just under not 150 bucks, but 1,500 bucks every month just fine. You won't even hit what you would do if you put $300 a month in for 40 like this is, this is where the math adds up. This is where time is on your side and this is where you know what, there's going to be years when you lose money, right? If you were in the market or you had one of these accounts of four oh one k account in 2008? Yes. What that four, oh one count maybe went down to a one-on-one accounts, you know, you know what I'm saying? Oh, an account or whatever, you know, like got cut in half. But as you continue to stay in the market, you know, I was doing real estate at the time. A lot of people were asking me, I lost half my money. What do I do? Six stay in, leave it alone. The government bailed us out like it's going to go back up. And most of them got back returns the next year. So yes after expansion comes recession, but after recession come to expansion, you know,

Speaker 2: 37:25 So that was the thing. When you have a target in mind, you have a goal in mind. You're not worried about these day to day things that are happening. You're not panicking saying, oh my God, like this past December, people started freaking out. This is just a month. It's just a few weeks. Things are going to, there's ebbs and flows. I know I'm staying true to the course. I said, I know what I need to do every month. No matter what happens in the end, I know I'm going to get to my goal.

Speaker 3: 37:53 All right. Any other scenarios where you want to run?

Speaker 2: 37:57 No, I think, I think we ran through some fun scenarios for people to, to, to know. I think, I think hopefully one of the most eyeopening scenarios is you sacrifice five years, you max out and in the next 30 you can not contribute. If you wanted that plan and you could be okay.

Speaker 3: 38:22 Yeah, that's true. That's true. Or the the opposite. If you're in the millennial category, you got time, three, 300 bucks a month. Yeah. 300 bucks a month. We'll get you one point 9,000,040 years. Yeah. If you want to go with 200 that's just running, maybe we're just running that scenario. 200 bucks a month, just in case forever one for 40

Speaker 4: 38:50 And you could still have a $36,000 a year lifestyle.

Speaker 3: 38:53 Yeah. You know, I'm sure. Oh, is that what it came down to? Yeah. To see the, and that's the crazy part, right? You put away $200 a month for four years, and that's the same as putting away $19,000 a month. I mean, $19,000 a year

Speaker 4: 39:14 For five years or five years. 200 versus 1500 mm. Like let's, let me see this. Let's, let's do 20 to 25 Max contribution and then from that on 100 bucks a month.

Speaker 1: 39:30 Okay.

Speaker 4: 39:31 And this is for, what does that come up? 2025 is 19,000 and for the rest of your life, you're just doing a hundred bucks a month. 100 okay. Yeah. So you're not, you're not quitting, you're just putting like a bare minimum maintenance kind of amount of money in there. So first five years you're not get out and then you just do 1200 a year for the rest.

Speaker 1: 39:57 Okay.

Speaker 3: 40:04 Well, but again, you know, that's the whole thing about [inaudible] this,

Speaker 4: 40:07 There you go for three mil.

Speaker 3: 40:09 Yeah. But see that's the part where it adds up year after year after year after year.

Speaker 4: 40:15 Yup. The sacrifice those first five years. And then you just put in a bare minimum, 100 bucks and 20, 20, 60, you'll have four, three in theory.

Speaker 3: 40:26 Right. And then, and again, this is with time on your side. [inaudible] Not everybody has, you know, time like this for years. I know I don't have four years, but you know, wow. You know, it's, it just kind of depends where you're at. So no, for those of you that are listening to this podcast, I know it's hard for you to see us manipulate the excel spreadsheet. But maybe if you go home and you watch the video and kind of see how we're manipulating it. The other thing I want to show people how to change is basically this row has a formula of the percentage. So if you wanted to change this to 8%,

Speaker 4: 41:02 Yeah. So for you guys on a podcast, so we're just clicking on that top, top row there, and then you see the column times a percentage. So right now it's 0.8, so that'd be 8% interest. Yeah. So you can,

Speaker 3: 41:15 You can change that. But then again, you know, and then from there, the box that you highlight has a little tiny square in the bottom. We just grabbed that and then real quick,

Speaker 4: 41:25 Well it all the way though,

Speaker 3: 41:27 I'll change it. You know. So you know, if you're one of those skeptics out there that you think 8%, I mean 10% is too much.

Speaker 4: 41:37 Yeah. You're still looking at that. Somethings wrong cause that's trillions of dollars. Maybe a 0.8 sorry, zero zero eight. Sorry. Yeah, that's okay. When you start to see funky things for their life. But yeah, 0.08 trillions of dollars cause we didn't, we didn't change it on the go change. Yeah. Can you yeah, you just change it for at the top drag the 10 day ago, 2.16 mil.

Speaker 3: 42:04 You know what I'm saying? Like, if you think 10% is not enough, then you know, and again, if you think that's not what you want to change it to 5% and this is 5% and starting at the whole, if you want to Max it for the first five years, then put a hundred bucks the rest of your time, the time, okay. 5%. You know, you're getting close to a mill. But again, like, you know, we can play with these numbers. We're showing you how to change it 5% all the way down. But in real life, if you wanted to keep track of it, this would be 5% right? And then this one would be 8% or 10% right? Right.

Speaker 4: 42:46 But this year we had a 12% growth,

Speaker 3: 42:48 That kind of stuff. And then you can put, you know, negative effects in here and you can change your contribution. So if you want to get really technical like we all like to get technical, you can kind of lay with this how you see fit. So, but anyway, but just

Speaker 4: 43:05 So, go ahead. I'm sorry. I like to ransom likes to get granular with it. I like to just do something like this. It's like 100 bucks a month. K sounds good. I'll reevaluate. And in six months I'll reevaluate in a year. And that's how I, I like to do things such as simple and just keep it cut and dry and then I just move on with my life. Yeah. So I mean, just

Speaker 3: 43:25 Again, sorry for those of you that are listening to the podcast, but again, if you're interested and you're listening to some podcast, just go on and click on the show notes when you get home and you know, you fast forward the youtube video or the video that you're watching it or whatever source you're doing and just kind of see how we're planning with the sheet. Also if you guys have questions, don't, don't forget to email us or contact us, leave comments, apps, whatever we want to do, you know, but we just want to put knowledge out there and make people aware of like, Hey, you know, these are things that you can do. We want to talk about all kinds of things in the show, not just things that are geared towards business. You know, this is for the everyday person like that. We gave that example, the 25. He made 36,000 a year. I'm never gonna amount to anything. Now you're wrong. You can change your life.

Speaker 4: 44:14 Change that thought and taking the ball. Yeah. It doesn't have to be complicated. And the thing I like about this is you can start to see yourself winning. You can start to see progress. You can start to see these things that make it hard sometimes. And you feel like you're just flooding your head up against a wall. Like, I got student loan debt, I got this car payments. Just say only you look at this and you start to do it. And you say, seeing what I'm winning here. And I know when I look out at my future, I know I'm going to be okay. I know things are going to be okay. I know I'm going to have money. It's sucking now. Maybe, maybe I gotta go from, from Louis Vuittons I got to come down the Nike's and then, you know, one day I can go back up.

Speaker 4: 44:57 You know, you gotta meet those things and understand this and I think like I said, this helps, helps you to when helps you to start to see success happening and really get your momentum moving. And once you get these habits built, you know, then then, then, then you'll start stop thinking about yourself. Stress less about these things, get those habits built, use systems to automate things. Most employers will take this money out for you. You know, you can automate things when you get paid to just go places. There's lots of tools for you guys out there. I said different things you can use to help make this stuff out of sight, out of mind kind of things. That really helped a lot, especially with money. If you, if you got 1200 bucks in your account and that even though maybe somewhere else you've had another thousand go somewhere else, you're not seeing that necessarily. If you can keep that out of your mind. It's like getting used to the new found amount you're going to live on knowing this and I'm going to put this away like this. I see where I'm going to head in the future. And you go about your life that way.

Speaker 3: 46:00 Yeah. Anything else? No. Again, that's just, you know, I, I was thinking about it one day and I was like, hey man, let's just make this sheet. Let's make it available for people as play around with it. And you know, that way people can start to come up with a plan and start to think about their future. You know, this isn't just, you know, something that is gonna come your way one day and be like, oh no, I gotta retire. What do I do? Like, because I think for this right here, right now, right after the show, pick it up, started doing it.

Speaker 4: 46:36 Absolutely. I hope this was fun. I had fun. This, to me, this is kind of fun to look at things and play with stuff and throw some different numbers in scenarios. I'll be, you guys had a good time. If you wanna look back, why, so youtube video, see how we're doing things. Like I said, ransom said earlier and we said before and you need help, please reach out. We want to help you guys. You know, whether it's manipulating the sheets or questions or whatever and the experts, but we'll either find them or pointing the right direction to find them. Some good resources on this we've put together in this particular show notes a lot there, factors to new good book. We're going to review reviewing that next week. So stay tuned for that book review. A new podcast that I've been really loving on this subject from guys that really are more experts than, than we definitely are.

Speaker 4: 47:26 Our polar pants. Afford anything. If you guys remember the movie I got turned on to that podcast and I've been really digging it up and loving it. I've been thinking about these things in a different way. The sheet will be available for you guys to to, to download or copy over to your Google stuff or whatever it is. I'll also leave links to past episodes. We've talked about a lot of different things around this subject. Please check those out if you haven't. There's within those, there's also links to relevant things in that episode, whether it's books or resources, websites. Please check those out. They're here for you guys.

Speaker 3: 47:59 Yeah. One of the other books I want to recommend on this subject too is Tony Robbins unshakeable book. Absolutely. Absolutely. He talks a lot about, you know, this process and how in today's world ETFs are probably a lot more, I guess, profitable. They don't take as many fees out of your account, the easier to manage and Nicholas Trades and mutual funds. But that's definitely a good good book to read. A Tony Robinson shakable. Absolutely.

Speaker 4: 48:27 And then for this month's giveaway, please head over to a social community.show/pick me every month where we're hard at work in the background or putting together different things, whether it's books, packages, sets, kits, whatever it is that we've come up with that we think is going to help you guys. It's helping us in our lives, helping us become better humans. Parents, friends, neighbors, brothers, sisters, whatever it is helping us get better. We want to pass it on to you, whether it's it's value, whether it's something to make your life better, make your life more efficient. Hetero switch, chameleon.show/pick me. Get into this month's giveaway. If you know something or know somebody that a product or whatever it is that we, you want us to check out, please let us know. Happy to check it out and see what we can work out for you guys and over there, check out what we got going on.

Speaker 4: 49:13 And then for this week's challenge, I want to see action. I want you guys to do something. You're not doing something. I was one of those guys. I was like, you know what? I don't need to do this stuff. I don't need to be saving. I'm going to be rich and I don't need that. Boyd, I was just a bad idea. I could, I really blew a lot of years. I'm not putting these small amounts in. I want you guys to take that minimum amount in a on a fun little thing that we learned. Taking that first hour of your work for yourself. So if you make 10 bucks an hour, you take that $10 every day, that's yours. And they also nothing and nobody else. So every week that's 50 bucks a week, 20 bucks a month. I think we ran through that scenario and what that looks like.

Speaker 4: 49:52 So there you go, go back if you want to rewind and see that what that winds up being, but take that first hour for you. Keep that in your pocket. I know it can be hard. I know it sounds crazy. Tasting 50 bucks a week. I can't even, I can't even put together 50 cents a week. It's tough. But you've got to start, start with whatever the minimum is for you. And if you are doing something already, this, let's see, 10% more, I see 1% more. Let's start stretching yourself. Use these formulas, plug that in. Challenge Yourself. This week's challenge is to, is to get action, take action, go do it guys passionately. And then that takes us to our final thoughts. You know, retirement is all about time, so if you're in the younger generations, time is on your side. Start now, keep it up, keep up the good work.

Speaker 4: 50:41 If you're in the later years and you know you kind of get defeated by what the five year returns look like, you know what? I guarantee you if you just get started, you know I guarantee you with the experience that you have, whatever experience that may be, just get started. When you start looking at things, when you start breaking down things, you'll start to figure it out. Believe me, just get started, Erin. That's just one source guys. That's just one source of things. You can always do. Other things and speaking of doing other things, if you've got friends, colleagues, brothers, sisters, neighbors, cousins that these compare this are, you guys have been talking about it and shared this with them. I have a conversation. You guys walk through some things that that's the best way to help yourself. Help the show to share and pass the information on.

Speaker 4: 51:24 Spread the message of good things. If you, if you like what we've got going on, leave a review. If you don't like we got going on, leave a review. Let us know between shows. You guys can catch us, the social community and show on Facebook, Instagram, Twitter. You can describe on the Youtube or your favorite podcast app or past episodes and everything we talked about here today. You can visit a social chameleon.show. Until next time, keep learning. Keep growing. Not just yourself, but your bank account, your savings and transforming into the person you want to become.

Speaker 1: 52:23 [Inaudible].

This podcast is available on…